| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 45,479.60 | -878.82 | -1.90% |

| S&P 500 | 6,552.51 | -182.6 | -2.71% |

| Nasdaq | 22,204.43 | -820.2 | -3.56% |

| VIX | 21.66 | 5.23 | 31.83% |

| Gold | 4,035.70 | 35.3 | 0.88% |

| Oil | 58.24 | -0.66 | -1.12% |

OVERVIEW OF THE US MARKET

Wall Street tumbled on October 10, 2025, as renewed US-China trade tensions from President Trump’s tariff threats triggered a rush to safety, with the S&P 500 plunging 2.71% to 6,552.51 in its worst day since April. The Nasdaq Composite sank 3.56% to 22,204.43, led by tech’s 3.97% drop, while the Dow Jones Industrial Average fell 1.90% to 45,479.60. Nvidia dropped 4.89% on heavy volume amid AI bubble fears, and Plug Power declined 9.52%. Consumer staples rose 0.25%, bucking the rout.

The selloff erased weekly gains, with information technology hardest hit as tariff hikes threatened supply chains. Recent data showed August trade deficit at -$78.3 billion wider than expected, factory orders down 1.3% versus 1.4% poll, underscoring vulnerabilities. September non-farm payrolls, due Friday but delayed by shutdown, had a 50,000 add forecast after August’s 22,000, with unemployment at 4.3%.

Interactive Brokers’ Steve Sosnick calls it a “tariff rug pull” amid complacency, JonesTrading’s Michael O’Rourke warns of larger correction if truce ends. 22V’s Michael Hirson sees backdown window but political risks for Trump. Northlight’s Chris Zaccarelli expects rebound absent economic hit, dip-buyers vindicated by year-end. FBB’s Michael Bailey views tariffs as cover for AI selling. Janney’s Dan Wantrobski anticipated 5-10% pullback from overbought, not structural downturn. Fundstrat’s Mark Newton suspects further Fall selloff despite bounces. Allianz’s Charlie Ripley notes threats not always actions, fundamentals intact.

Bank of America cites $20 billion equity inflows, $25.6 billion bonds, $5.5 billion crypto, ample dry powder. Comerica’s Eric Teal advocates diversification amid concentration.

Corporate highlights included Tesla’s Shanghai shipments up, Google’s UK strategic status, China fees on US ships and Qualcomm probe. Chevron seeks Namibia wells, Mosaic phosphate shortfalls. CoreWeave leaders sold $1 billion shares. AstraZeneca nears Trump drug price deal, Stellantis shipments up 13%. Carlyle takes BASF coatings, BlackRock funds accept BBVA Sabadell bid.

Ahead, next week’s earnings amid trade jitters.

OVERVIEW OF THE AUSTRALIAN MARKET

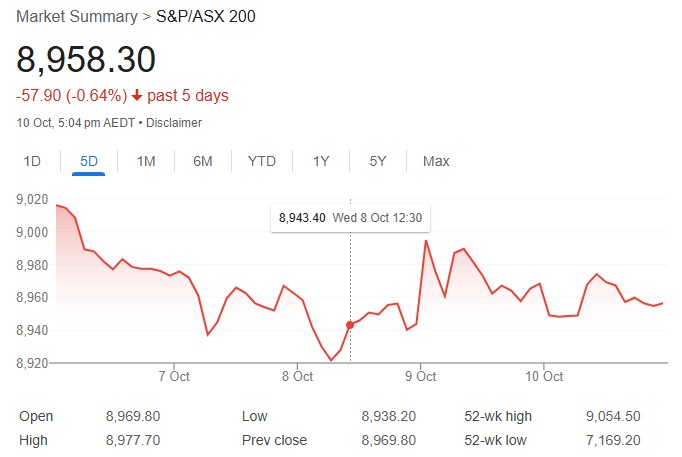

Australia’s share market closed lower on October 10, 2025, capping a 0.32% weekly decline as materials slumped 2.10% on gold, copper weakness, dragging the S&P/ASX 200 down 0.13% to 8,958.3 and All Ordinaries off 0.13% to 9,264.3. Information technology rose 1.11%, consumer discretionary up 0.73%. Novonix surged 27.3% on graphite production, Focus Minerals up 20.2%.

Gold sub-sector fell 3.5% as prices eased from $4,059 peak, despite 93% YTD gain. September inflation expectations at 4.8% vs 4.7% curbed RBA cut bets. Energy down 0.73% on oil dip amid Gaza deal.

Standouts: L1 Group up 16.2% on AUM update, European Lithium gaining 15.4% on offtake. Painchek dropped 13.3% post-rally.

AMP’s Shane Oliver sees correction risk from valuations, triggers, but positive 6-12 months on Trump pivot, Fed cuts, RBA easing.

Ahead: RBA minutes Tuesday, jobs Thursday hinting inflation path.