Summary

Sanae Takaichi’s victory in the Liberal Democratic Party (LDP) leadership race on October 4, 2025, triggered what markets call the “Takaichi Trade.” Investors anticipate bold fiscal expansion and continued monetary easing as she prepares to become Japan’s next prime minister. Her pro-growth stance sparked a record surge in Japanese equities, rising JGB yields, and a yen depreciation beyond ¥150 per U.S. dollar, signaling expectations of aggressive spending, infrastructure stimulus, and a long-term economic reorientation toward domestic revival and structural reform.

Market Reaction: The “Takaichi Trade”

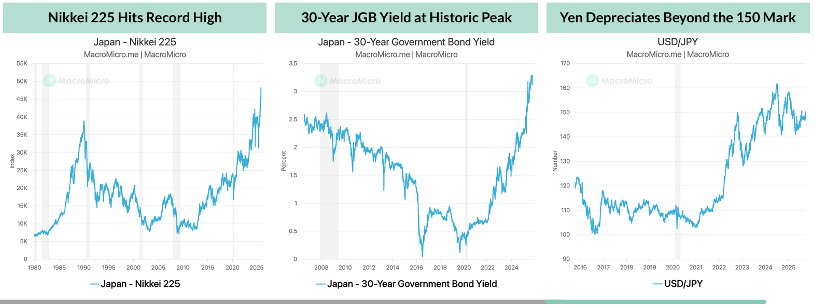

On October 4, 2025, Sanae Takaichi defeated Shinjiro Koizumi to become the new LDP leader and the expected next Prime Minister of Japan, pending the Diet’s mid-October confirmation vote. Financial markets immediately priced in a new “fiscal reawakening”.

- Equities: The Nikkei 225 surged to record highs, signalling strong investor confidence in her pro-growth stance.

- Bonds: Japanese Government Bond (JGB) yields climbed to new peaks, reflecting expectations of heavy government borrowing to finance stimulus.

- Currency: The yen weakened beyond ¥150 per U.S. dollar, underscoring the perceived continuation of ultra-loose monetary policy. Investors interpreted her victory as a catalyst for a policy mix that combines aggressive fiscal expansion with dovish monetary policy—mirroring a “high-pressure economy” approach aimed at raising nominal growth through sustained demand.

Exhibit 1: Repricing of Japanese Assets

Policy Blueprint

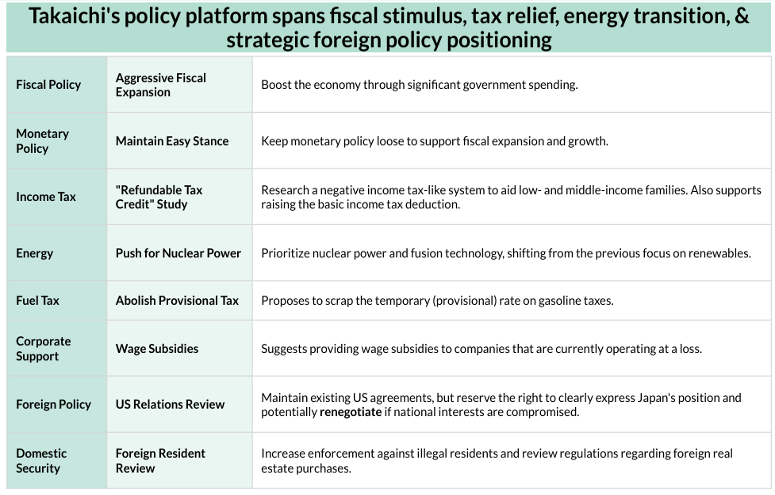

Takaichi’s economic blueprint is anchored in her doctrine of “Responsible Aggressive Fiscal Policy,” which emphasizes supporting middle- and working-class households while reinvigorating domestic demand and productivity.

Key components include:

- Fiscal Stimulus: Commitment to deficit-financed expansion focused on National Resilience infrastructure and public works to strengthen growth and employment.

- Tax Relief: Proposals for a Negative Income Tax system (refundable tax credits) and higher income deductions to support low- and middle-income families.

- Corporate Reform: Plans to mobilize idle corporate cash reserves, potentially through taxation or governance reforms, to encourage business investment and wage growth.

- Energy Policy: A decisive pivot toward nuclear and fusion energy, reducing reliance on costly renewables and imported fossil fuels to narrow Japan’s trade deficit.

- Monetary and Social Policy: Maintaining a loose BOJ stance to support expansion, while lowering social insurance premiums to ease household financial burdens.

Her foreign policy remains anchored in the U.S.–Japan security alliance, though she intends to assert Japan’s economic independence in trade negotiations and safeguard national interests, including through stricter foreign real estate and residency regulations.

Exhibit 2: Takaichi’s Policy Platform

Yen Dynamics and BOJ Policy Outlook

Following Takaichi’s election, market expectations for a BOJ rate hike declined sharply—from 57% to 24%—as investors anticipated continued monetary support for her fiscal expansion plans. Despite this, BOJ officials maintained that inflation is improving, and rate hikes remain on the horizon, with interest-rate futures implying an upward bias through 2026.

Interestingly, the yen has remained weak even though the U.S.–Japan yield differential has narrowed to a three-year low. Analysts note a historical pattern in which the yen typically begins to appreciate 1–2 months after such a narrowing, suggesting potential for a delayed yen rebound once markets re-price interest-rate expectations. Combined with anticipated Federal Reserve rate cuts in 2026, the yen may strengthen in the second half of 2025. This phase marks a divergence between Japan’s domestic yield trends and its currency movements—a setup often preceding yen appreciation cycles.

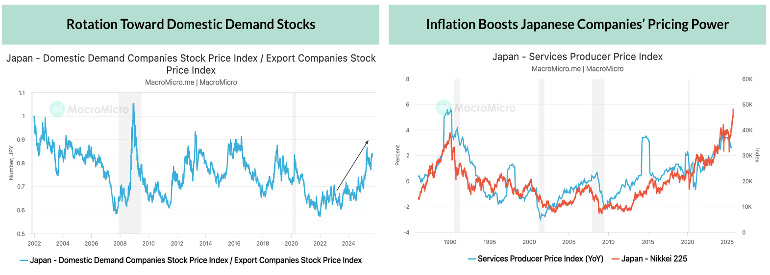

Market Rotation Toward Domestic Demand Stocks

Japan’s equity rally has entered a new phase marked by a rotation toward domestic-demand sectors. Previously, export-oriented firms benefited from yen weakness; however, tariff pressures and slowing global demand have eroded their performance. Instead, domestic industries—such as retail, construction, and services—are driving gains, supported by rising inflation and strong pricing power. The Corporate Services Price Index remains near a 10-year high, signalling improved corporate margins and sustained inflation pass-through. This shift suggests Japan’s growth is becoming more internally driven, underpinned by fiscal expansion, higher wages, and resilient domestic consumption rather than export reliance.

Exhibit 3: Domestic Rotation and Pricing Power