| Close | Previous Close | Change | |

|---|---|---|---|

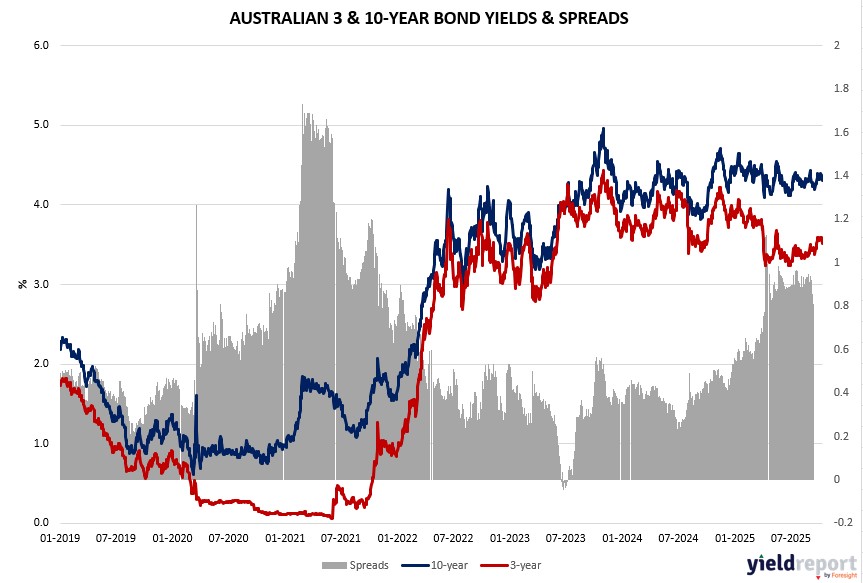

| Australian 3-year bond (%) | 3.519 | 3.591 | -0.072 |

| Australian 10-year bond (%) | 4.293 | 4.371 | -0.078 |

| Australian 30-year bond (%) | 4.966 | 5.022 | -0.056 |

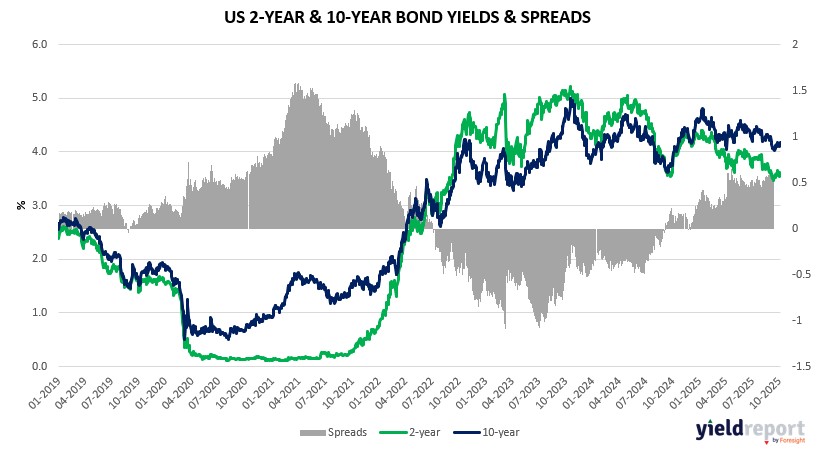

| United States 2-year bond (%) | 3.522 | 3.585 | -0.063 |

| United States 10-year bond (%) | 4.051 | 4.115 | -0.064 |

| United States 30-year bond (%) | 4.634 | 4.6938 | -0.0598 |

Overview of the Australian Bond Market

Australian government bond yields edged lower on October 13, 2025, with the 10-year yield down 8 basis points to 4.28%, tracking risk aversion from equity declines and US-China frictions. The 2-year yield fell to 3.46%, while the 15-year dipped to 4.61%, as traders sought havens amid trade uncertainty.

Macro pressures mounted with China’s stance on rare-earth curbs potentially blunting tariff impacts, though Beijing’s export surge to a six-month high bolsters its leverage. Locally, the Aussie dollar rose 0.78% to 0.6525 against the US dollar, but broader sentiment remains cautious ahead of RBA September minutes Tuesday and labor data Wednesday, which could influence rate cut bets if unemployment ticks up. Investors anticipate steady policy amid inflation control, with pullbacks seen as opportunities if fundamentals hold, per strategists, though earnings volatility and AI outlooks pose near-term risks.

Overview of the US Bond Market

Bond trading was subdued on October 13, 2025, with the US market closed for Columbus Day, leading to minimal movement in Treasury futures and the 10-year yield holding steady around 4.03%. Longer-dated yields saw slight adjustments, with the 30-year at 4.62%, as investors weighed the resilience of the bull market against upcoming economic data that could influence Federal Reserve policy.

The dollar’s 0.2% gain reflected risk-on sentiment from equity rebounds, but macro uncertainties persist, including potential tariff escalations if US-China talks stall. Bessent indicated staff-level meetings this week could address rare-earth exemptions and export controls, with all options open ahead of the Trump-Xi summit. Analysts at Nomura suggest both sides have incentives to avoid derailing negotiations, given China’s export strength and US farmer pressures.

Looking ahead, this week’s data releases could sway rate expectations, with retail sales and housing starts due Thursday, potentially signaling consumer and economic health. Philly Fed business index and import prices follow Wednesday, while non-farm payrolls on Sunday may test labor market stability amid forecasts of 50,000 job gains and a steady 4.3% unemployment rate. Bond traders have trimmed long positions in recent weeks, per JPMorgan surveys, with asset managers paring net longs across tenors by a combined equivalent of $23.5 million per basis point in prior data, reflecting caution on valuations and Fed dissent risks. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance, as the economy dodges recession signals.