| Close | Previous Close | Change | |

|---|---|---|---|

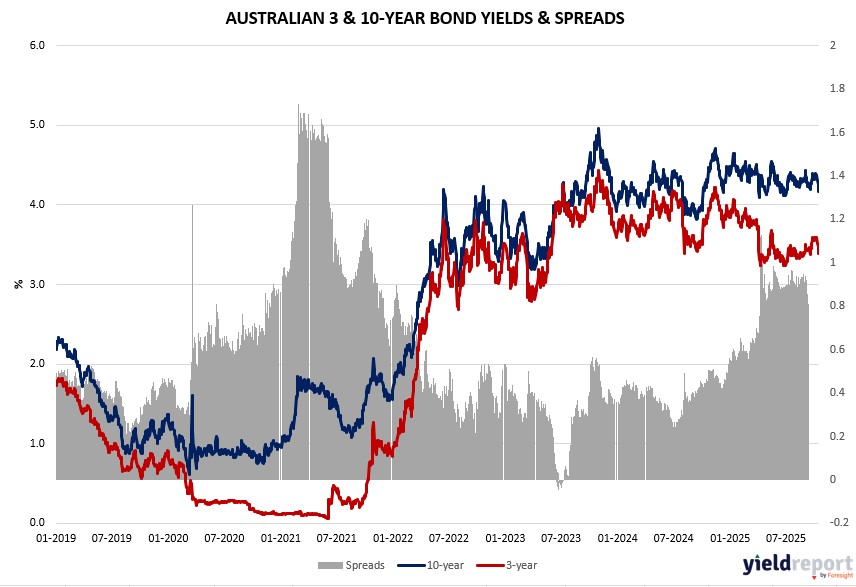

| Australian 3-year bond (%) | 3.314 | 3.393 | -0.079 |

| Australian 10-year bond (%) | 4.099 | 4.17 | -0.071 |

| Australian 30-year bond (%) | 4.837 | 4.866 | -0.029 |

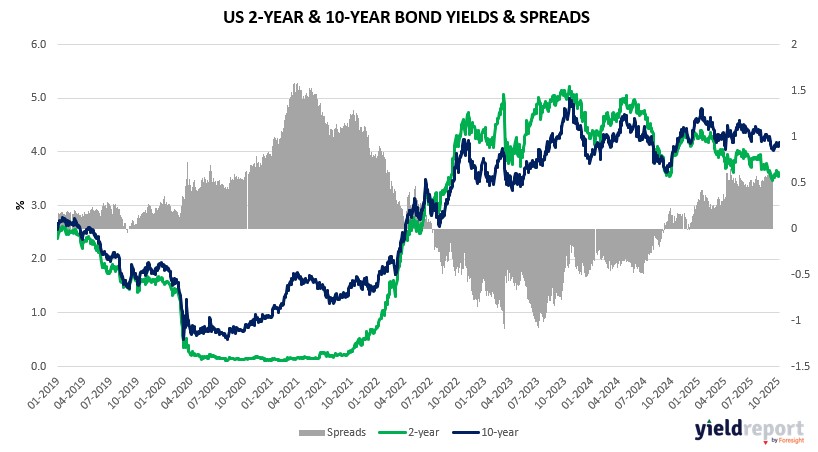

| United States 2-year bond (%) | 3.393 | 3.495 | -0.102 |

| United States 10-year bond (%) | 3.3957 | 4.022 | -0.6263 |

| United States 30-year bond (%) | 4.5768 | 3.6129 | 0.9639 |

Overview of the Australian Bond Market

Australian government bond yields rose modestly, with the two-year up four basis points to 3.32% and the 10-year advancing four basis points to 4.13%, as rotation to banks amid mining pullback reflected bond proxy strength. The five-year increased four basis points to 3.54%, and 15-year rose two basis points to 4.48%. The Aussie dollar strengthened 0.16% to 0.6506 versus the US dollar, buoyed by US-China de-escalation hopes and critical minerals deal.

Albanese-Trump agreement on rare earths and minerals, with $8.5 billion pipeline and protections against unfair trade, eases concerns over China’s export curbs, potentially stabilizing supply chains. Trump’s confidence in fair US-China deal, despite tariff threats, supported risk appetite, though soybean frustrations and fentanyl demands underscore tensions.

Softer gold and iron ore weighed on resources, but financials rally signals resilient sentiment. Upcoming flash PMIs Wednesday forecast at 51.4 manufacturing and 52.4 services/composite, indicating moderate expansion amid trade dynamics.

Overview of the US Bond Market

Bond yields dipped as Treasuries gained, with the 10-year yield falling three basis points to 3.98% and the 30-year declining three basis points to 4.57%, reflecting eased trade war fears and solid earnings offsetting shutdown-induced data gaps. The two-year yield held steady at 3.46%, while gold surged 3% to $4,377.50 an ounce on safe-haven bids. The dollar edged up 0.1%, pressuring the euro and pound slightly.

Trump’s comments on expecting a great trade deal with China, despite threats of tariff hikes and airline parts curbs if no agreement by November 1, buoyed sentiment, with soybeans and rare earths central to demands. His sidestep on Taiwan concessions and emphasis on fentanyl curbs highlighted divisive issues, yet plans for Xi meeting next week suggested de-escalation potential. Treasury Secretary Bessent’s confirmation of Malaysia talks this week added to hopes for truce extension.

Economic resilience amid trade frictions supports views of rates higher for longer, though Fed cut bets persist. Rick Gardner anticipates an October reduction despite volatility, with TD Securities’ Oscar Munoz forecasting September core CPI at 0.3% monthly—due Friday after delay—due to cooling services offsetting tariff-driven goods inflation, likely prompting a 25-basis-point cut amid labor risks.

JPMorgan’s client survey showed shrinking net longs to two-month lows, indicating caution ahead of CPI and earnings. Asset managers trimmed net longs in Treasury futures by $23.5 million per basis point, focused on 5-year and bonds, while leveraged funds pared shorts in longer maturities per CFTC data.

Dealers expect steady coupon sizes for November-January, with 10-year at $42 billion and 30-year at $25 billion, aligning with guidance.