| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,924.74 | 218.16 | 0.47% |

| S&P 500 | 6,735.35 | 0.22 | 0.00% |

| Nasdaq | 22,953.67 | -36.88 | -0.16% |

| VIX | 17.87 | -0.36 | -1.97% |

| Gold | 4,135.30 | 26.2 | 0.64% |

| Oil | 57.86 | 0.34 | 0.59% |

OVERVIEW OF THE US MARKET

Wall Street ended mixed on October 21, 2025, as the S&P 500 closed little changed near record highs amid signs of buyer fatigue, while gold and silver suffered steep losses that overshadowed the session. The Dow Jones Industrial Average climbed 0.5% to a new all-time high, boosted by strong outlooks from companies like 3M, whereas the Nasdaq Composite dipped 0.2% as tech giants faced pressure. Consumer discretionary stocks led gains with a 1.3% rise, driven by resilient spending signals, but communication services fell 0.9% after Alphabet sank on competition from OpenAI’s AI-powered browser.

Gold tumbled 5.7% in its biggest drop in years, pulling back from recent highs amid profit-taking, a stronger dollar, and improved US-China trade talks, with analysts viewing the correction as healthy but warning of potential further volatility. Silver slumped even more sharply, down 7.1%, following a historic squeeze in London and outflows from Shanghai vaults. Equities showed resilience despite these moves, with hedge funds maintaining high stock exposure per Barclays data, though strategists like Piper Sandler’s Craig Johnson called for a near-term pullback to consolidate gains.

Corporate earnings provided a mixed backdrop: Netflix reported a tax hit from Brazil, Texas Instruments issued a tepid forecast, and Mattel missed estimates due to tariff uncertainties, while General Motors, Coca-Cola, and General Electric raised outlooks on robust demand. Bitcoin edged up 0.6% amid broader crypto stability. Investors are eyeing the Federal Reserve’s October 29 rate decision, with most-shorted stocks on track for their best October since 2008, signaling dip-buying opportunities as noted by Pepperstone’s Michael Brown.

The session highlighted ongoing credit concerns in banking, with Goldman Sachs’ David Solomon downplaying regional bank frauds as isolated, even as Zions Bancorp reassured with better-than-expected profit. With the US government shutdown creating data gaps, including delayed CFTC reports on positioning, market participants remain cautious on precious metals, where volatility against the S&P 500 hit pandemic-era levels.

OVERVIEW OF THE AUSTRALIAN MARKET

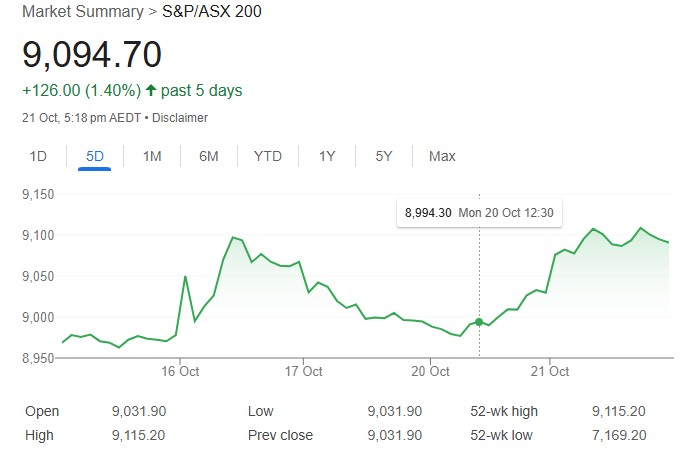

The Australian share market advanced on October 21, 2025, with the S&P/ASX 200 closing up 0.7% at 9,094.7, led by a rebound in resources amid broader strength in critical minerals and precious metals. Materials stocks jumped 1.7% as majors like BHP rose 2.3% and South32 gained 4.5%, while the gold sub-index climbed 2.3% with Evolution Mining up 4.4%. Communication services and health care also rose over 1%, but consumer staples slipped 0.3% in a session of solid breadth, with 181 advancers versus 92 decliners in the ASX 300.

Fund flows favored resources after months of underperformance, spotlighting critical minerals like rare earths and lithium, where stocks such as VHM surged 20.7% on export finance support and Astron jumped 22.9% on project backing. General strength in precious metals lifted names like G50 Corp up 19.6%, while tech held flat and energy eked out a 0.1% gain. Standouts included Hub24 up 10.6% on a positive Q1 update and Praemium rising 7.8% after strong quarterly figures, contrasting with pullbacks in recent high-flyers like Manuka Resources down 23.7% on a capital raise.

The rally came amid global cues like falling gold prices, but local resilience was evident, with IMARC presentations boosting miners like Australian Strategic Materials up 8.3%. Investors await S&P Global PMI flashes on October 23, which could influence sentiment on manufacturing and services after last month’s readings around 52, as tariff uncertainties and China talks remain in focus.