| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.371 | 3.367 | 0.004 |

| Australian 10-year bond (%) | 4.144 | 4.129 | 0.015 |

| Australian 30-year bond (%) | 4.832 | 4.811 | 0.021 |

| United States 2-year bond (%) | 3.497 | 3.463 | 0.034 |

| United States 10-year bond (%) | 4.01 | 3.989 | 0.021 |

| United States 30-year bond (%) | 4.5938 | 4.5749 | 0.0189 |

Overview of the Australian Bond Market

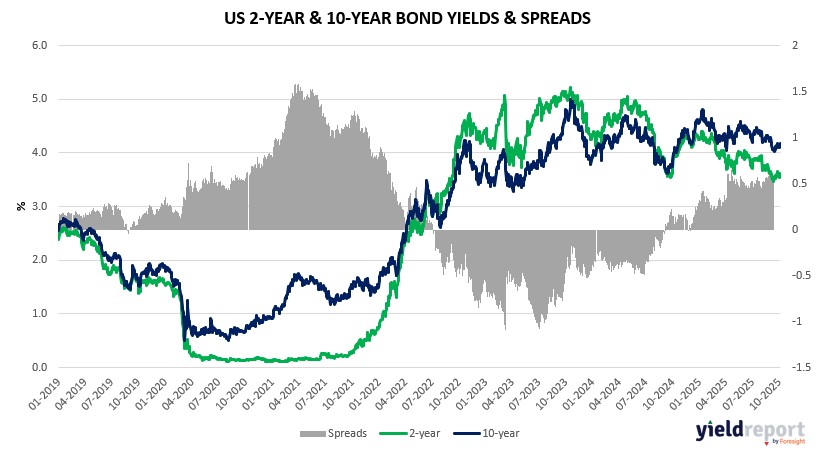

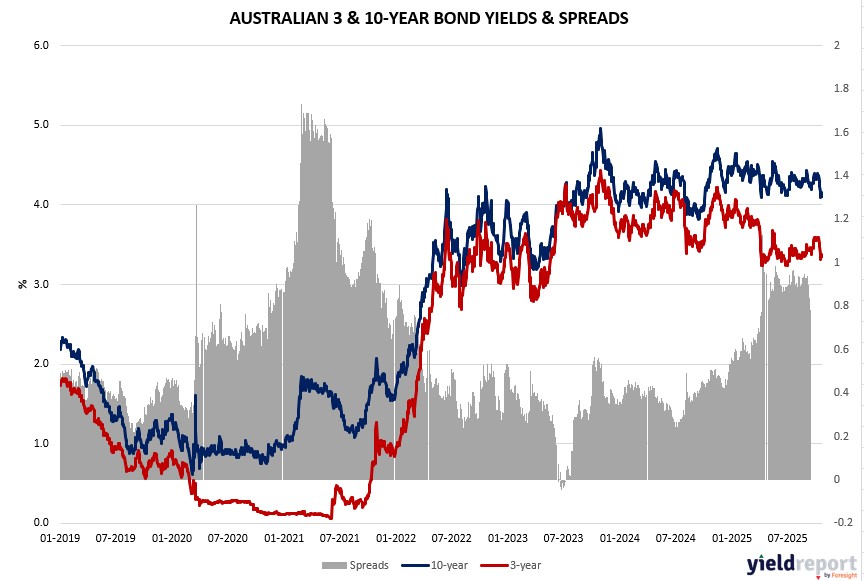

Australian government bond yields edged higher on October 24, 2025, with the 10-year up 2 basis points to 4.14% tracking US stability post-CPI, though AUD/USD down 0.2% at 0.6499 limited gains. Shorter 2-year rose 1 basis point to 3.34%, reflecting PMI mixed signals, while 15-year added 2 basis points to 4.47% amid global risk-on from trade talks.

Macro blends encompassed manufacturing PMI dip to 49.7—first contraction since May—balanced by services at 53.1, keeping composite expansion at 52.6, highlighting resilience per S&P yet uneven amid tariff uncertainties. Positioning cautious pre-local CPI and RBA speech, with US core’s softer 0.2% monthly reinforcing global easing, where Pacific’s Tiffany Wilding notes modest tariff passthrough from retail pressures anchoring expectations. Dealers expect steady auctions, as RBA monitors Fed’s likely October 29 cut and QT end per JPMorgan’s Feroli.

Oil dip aiding disinflation could bolster bonds if PMIs foreshadow slowdown, blending with NAB consumer stress and China pledges for self-sufficiency and consumption boost, potentially lifting exports.

Overview of the US Bond Market

Treasury yields were little changed on October 24, 2025, with the 10-year steady at 4.00% after an initial dip on soft CPI faded amid resilient PMIs, blending inflation relief with growth signals that cap aggressive easing bets. Shorter 2-year yields fell 1 basis point to 3.48%, reflecting dovish cut odds, while 30-year held at 4.59% as oil’s drop tempered tariff-induced price fears.

Macro influences included core CPI’s 0.2% monthly rise—below poll—keeping annual at 3%, with headline 0.3%, confirming sticky but fading trends per Lombard Odier’s Florian Ielpo, reinforcing multiple 2025 cuts amid anchored expectations. Consumer sentiment’s drop to 53.6 highlighted price erosion on finances, yet S&P PMIs’ uptick and existing home sales at 4.06 million—meeting poll—bolster labor-focused Fed narrative, per Morgan Stanley’s Ellen Zentner seeing no surge or cliff. Positioning via delayed CFTC likely shows trimmed longs, with JPMorgan’s Michael Feroli expecting QT end announcement October 29 alongside cut, viewing benign data as risk-management greenlight.

White House noted no October CPI due to shutdown, heightening private data reliance, where ClearBridge’s Josh Jamner flags slower goods inflation undershooting tariff expectations, aiding labor support. With swaps at 120 basis points easing to sub-3% neutral by mid-2026, bonds may see support if jobs weaken, though Strategas’ Don Rissmiller sees contained upside risks from anchored expectations despite utilities and used cars volatility.