| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,590.41 | -334.33 | -0.71% |

| S&P 500 | 6,699.40 | -35.95 | -0.53% |

| Nasdaq | 22,740.40 | -213.27 | -0.93% |

| VIX | 18.6 | 0.73 | 4.09% |

| Gold | 4,106.80 | 41.4 | 1.02% |

| Oil | 60.05 | 1.55 | 2.65% |

OVERVIEW OF THE US MARKET

Wall Street extended losses on October 22, 2025, as volatility resurfaced amid a momentum unwind in speculative assets and fresh trade anxieties from reports of potential US restrictions on software exports to China. The S&P 500 fell 0.5%, slipping below 6,700, while the Nasdaq 100 dropped 1% following tepid outlooks from Texas Instruments and a 10% plunge in Netflix. The Dow Jones Industrial Average declined 0.7%, with industrials down 1.3% as broader risk sentiment soured. Energy stocks bucked the trend, rising 1.3% on higher oil prices, but consumer discretionary and tech sectors lagged with losses over 0.8%.

Gold extended its rout, falling 0.5% after an initial 2.9% drop, holding above $4,100 amid choppy trading as investors digested overstretched rallies driven by debasement trades and Fed easing bets. Silver pared losses to end 0.3% lower, while Bitcoin slid 2.6% in a broader pullback for retail-favored assets like crypto and AI names, with the Bloomberg US Pure Momentum Portfolio reflecting sharp declines. Beyond Meat whipsawed amid meme-stock volatility, and Tesla slipped in after-hours despite record Q3 revenue, as profit missed estimates.

Corporate earnings showed resilience, with 87% of S&P 500 reporters beating expectations—the highest since 2021—bolstering views from JPMorgan’s Dubravko Lakos-Bujas that AI cycles and consumer strength support growth, though strategists like City Index’s Fiona Cincotta noted stretched valuations demand exceptional fundamentals. Southwest Airlines surprised with adjusted profit on bag fees, Alphabet touted quantum breakthroughs, and Capital One surged on buyback plans post-Discover acquisition. Geopolitically, Treasury Secretary Scott Bessent flagged ramped-up Russia sanctions, adding to trade jitters ahead of potential Trump-Xi meetings.

With the rally pausing two weeks from S&P highs, defensive staples and real estate gained over 0.4%, per Bespoke’s note on cooling parabolic enthusiasm. Investors eye October 23 existing home sales data, polling at 4.06 million for September, and the Fed’s October 29 decision, where Fundstrat’s Thomas Lee sees solid earnings and dovish policy driving toward a 7,000 S&P year-end.

OVERVIEW OF THE AUSTRALIAN MARKET

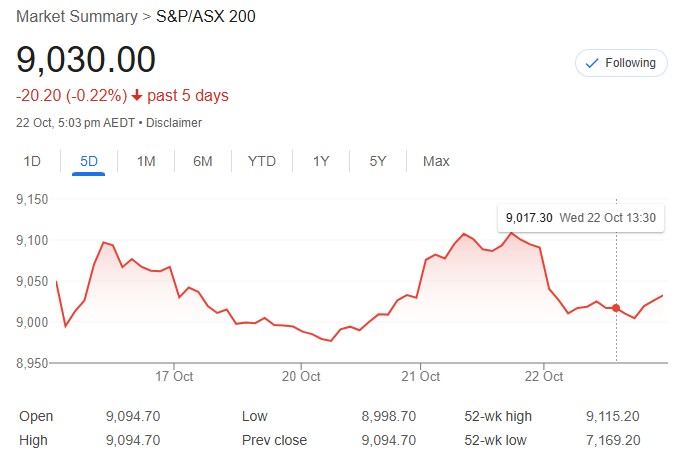

The Australian share market retreated on October 22, 2025, handing back prior gains as plunging gold prices triggered a mining sell-off, with the S&P/ASX 200 down 0.7% at 9,030 and the All Ordinaries off 0.7% at 9,321.1. Materials tumbled 3.1% amid gold’s rout, with the XGD sub-index plunging 8.5% as names like Nova Minerals fell 24.3% and G50 Corp dropped 14.1%; broader resources declined 2.7%, hitting Paladin Energy down 5.3% and Lynas Rare Earths off 3.3%. Energy provided the sole bright spot, up 1.3% on oil’s rise, led by Woodside’s 3.5% gain after improved Q3 production and guidance.

Fund flows shifted from precious metals—reminding of high-beta risks—to financials, which edged 0.1% higher with modest Big Four bank gains, while tech rose 0.4% amid rotations from low-PE resources. Standouts included Paradigm Biopharmaceuticals up 21.6% and Weebit Nano surging 18.9% on an investor update, with Northern Minerals gaining 14.5% on US funding support. Adairs jumped 8.3% despite cut guidance, citing reduced discounting, but consumer staples slipped 0.6% as NAB noted returning stress.

The dip followed Tuesday’s record close, with Moomoo’s Michael McCarthy attributing gold weakness to overbought conditions and impending US CPI, potentially flushing exuberance for a re-base. Investors await October 23 S&P Global PMI flashes, after prior readings around 52, which could gauge manufacturing and services amid tariff talks and China ties.