AI Investment Efficiency and Sustainability

After setting record highs, global equity markets have entered a volatile phase as investors debate whether the massive capital flows into artificial intelligence (AI) infrastructure will sustain earnings growth or erode profitability. The world’s largest technology firms—collectively the Magnificent 7—are at the core of this debate. Their escalating capital expenditures have created what some analysts describe as an “AI perpetual motion machine,” revolving around OpenAI and its expanding ecosystem

Tracking Capital Productivity in the AI Era – the Framework

To assess whether these enormous outlays are truly productive, we introduce the Computing Power Investment Efficiency (CPIE) indicator—a semi-annual measure tracking how effectively the Magnificent 7 convert capital expenditure (Capex) into usable computing power. The CPIE expresses the ratio between incremental computing capacity (in operations per second) and the total Capex over a given period. A higher ratio signals superior efficiency—more computational output per dollar spent—while a lower ratio indicates diminishing returns.

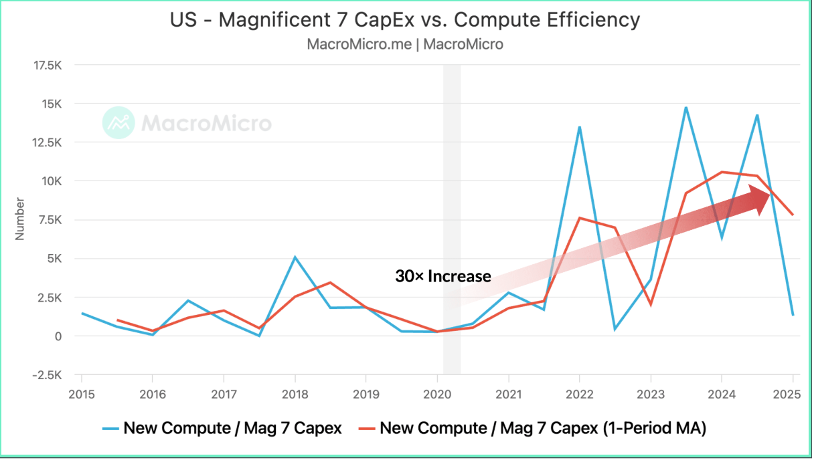

Exhibit 1 – Mag 7 Capex and Compute Efficiency

Computing power represents the capacity of hardware such as GPUs, CPUs, ASICs, and NPUs to execute data-intensive operations. These are typically measured in FLOPS (Floating-Point Operations Per Second). Capex, by contrast, captures the financial resources allocated to physical assets—data centres, semiconductors, and AI infrastructure.

The CPIE focuses on the “Magnificent 7”, the seven largest U.S. technology firms that dominate global market capitalization and AI investment: Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia, and Tesla. These firms have been at the center of what some analysts describe as an “AI perpetual motion machine” — a self-reinforcing ecosystem of innovation, infrastructure buildout, and reinvestment revolving around OpenAI and related platforms.

This indicator, updated semi-annually and based on a one-year rolling average, aims to track how effectively each dollar of Capex is being translated into incremental computing power. It reflects whether the ongoing surge in AI infrastructure spending is a sustainable growth driver or a potential profitability drag in the years ahead.

To understand CPIE, two fundamental components must be defined: computing power and capital investment.

- Computing Power measures the capacity of hardware systems to process data and execute calculations within a given time frame. It is typically expressed in FLOPS (Floating-Point Operations Per Second) — e.g., 1 TFLOPS equals one trillion operations per second. Higher FLOPS indicate superior capability in handling complex AI model training, scientific simulations, and high-precision computations.

- Compute Power Hardware includes GPUs, CPUs, ASICs, NPUs (AI accelerators), and advanced memory modules like HBM. These components collectively determine how efficiently systems can train and deploy AI models.

- Capital Investment represents total corporate spending on long-term physical assets — primarily data centres, semiconductors, and cloud infrastructure — all captured under Capex.

The ratio of incremental computing power generated to total Capex provides a measure of investment efficiency. A higher ratio means more computing power is produced per dollar spent, implying better use of capital resources.

- Measuring Compute Power Investment Efficiency

The CPIE aggregates data across the Magnificent 7 to calculate how much computing capacity has been added in the U.S. over a given period relative to total Capex outlays by these firms. This provides an industry-level view of how efficiently capital investments are being transformed into computational output — the foundation for AI productivity and, ultimately, profits.

According to recent analysis, the CPIE of the Magnificent 7 has increased more than 30-fold since 2020. This means that each dollar invested today produces roughly 30 times more computing power per second than it did five years ago. The finding highlights two important dynamics:

- Explosive growth in Capex as tech giants race to dominate AI infrastructure; and

- Substantial gains in capital efficiency, suggesting that these investments are yielding real, measurable improvements in computational performance.

The data supports the idea that since the onset of the AI era in 2023, these companies have entered a phase of sustained capital efficiency, successfully converting Capex into computing power, and computing power into productive capacity and revenue potential. In short, AI investments are not merely speculative; they are generating quantifiable improvements in technological leverage.

III. Emerging Risks and Signs of Plateau

However, recent trends indicate that this period of efficiency expansion may be reaching a plateau. The latest readings suggest early signs of stagnation in computing power investment efficiency. This may reflect the natural limits of hardware scalability, saturation of AI infrastructure, or diminishing marginal returns as spending continues to rise faster than performance improvements.

This potential slowdown serves as a critical warning: in an era of unprecedented capital intensity, monitoring the conversion efficiency of AI investments is vital. Without sustained gains in efficiency, escalating Capex could transform from a growth engine into a burden on corporate profitability and free cash flow.

- Implications for Investors and the Market

For investors, the CPIE acts as a forward-looking gauge of AI’s economic sustainability. A continued rise would signal that AI remains a transformative, productivity-enhancing force. Conversely, a downturn could indicate overinvestment and inefficiency — echoing the historical pattern of tech spending bubbles.

Our analysis shows that the Magnificent 7’s investment efficiency has risen over thirtyfold since 2020, meaning each Capex dollar now generates roughly thirty times more computing power per second. This surge reflects both exponential advances in hardware performance and the network effects of vertically integrated AI development—where cloud infrastructure, model training, and software deployment reinforce one another.

Since the onset of the AI boom in 2023, capital productivity in the sector has remained at historically elevated levels, underscoring that the transformation of capital into compute—and compute into profits—is real and measurable. However, the latest data reveal early signs of plateauing efficiency. As Capex intensity escalates, marginal returns on computing power are starting to flatten, suggesting the system’s self-reinforcing “perpetual motion” may be nearing physical and financial limits.

Monitoring CPIE will be critical for evaluating whether the AI ecosystem remains a durable growth engine or becomes an over-capitalized arms race. Sustained high efficiency would validate AI’s promise as a long-term productivity driver; deterioration could signal the dawn of capital discipline and consolidation across the AI value chain.

In sum, the Computing Power Investment Efficiency indicator provides a new analytical lens for understanding whether the AI revolution is creating enduring value or sowing the seeds of overcapacity. As the Magnificent 7’s Capex accelerates and the next CPIE update approaches, markets will be watching closely to see if the “AI perpetual motion machine” continues to generate real returns — or begins to show signs of strain.