Summary:

Australia’s labour market remains tight and inflation stubbornly elevated, prompting Reserve Bank of Australia (RBA) Governor Michele Bullock to signal a more cautious approach to further monetary easing following three rate cuts earlier this year. Speaking at an economists’ dinner in Sydney, Bullock said the central bank needs “a bit more data” on jobs and prices before making its next policy move, emphasising that monthly figures can be volatile.

Her remarks immediately reverberated through markets, with traders trimming bets on a November rate cut, the probability fell from about 60% to below 40%—and the Australian dollar strengthening 0.6% to US$0.6555, its highest level since early October. Bullock reiterated that the RBA board remains “cautious” and data-dependent, describing policy as still “a little bit restrictive” but not yet at a point where further easing is assured.

The comments come ahead of critical data releases, including the third-quarter CPI report, which will heavily influence the RBA’s November 3–4 meeting. Economists expect the trimmed mean inflation measure to hold at 2.7%, above the RBA’s August forecast of 2.6%, suggesting disinflation has stalled near the midpoint of the 2–3% target band. Bullock noted that a 30-basis-point upside miss on inflation would be “material” and could delay any additional cuts.

Analysts interpreted Bullock’s tone as less dovish. Commonwealth Bank economist Belinda Allen said the speech confirms the RBA will remain cautious and is unlikely to match the pace of rate reductions seen abroad, predicting the next move only in February 2026. Similarly, Goldman Sachs’ Andrew Boak said policy remains “contingent on the Q3 CPI outcome,” reinforcing the RBA’s emphasis on evidence-driven decision-making.

Bullock also highlighted that the RBA’s new staff forecasts, due next week, will guide the board’s judgment on whether the balance of risks favours further easing to support employment or holding steady to contain inflation. While she acknowledged progress in restoring price stability and preserving labour-market gains, she warned against “counting the chickens too soon.”

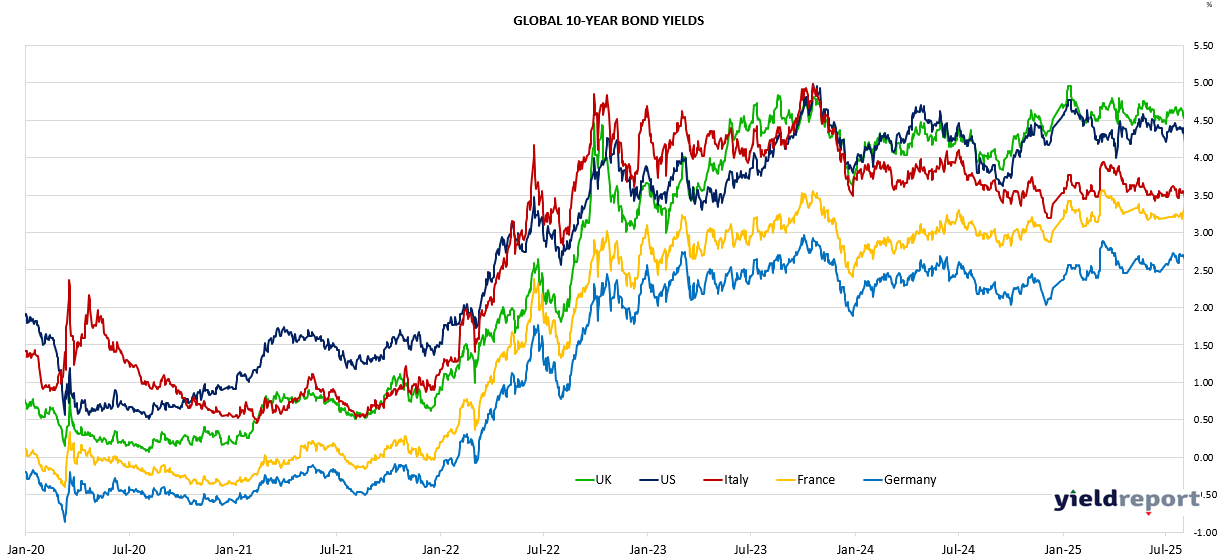

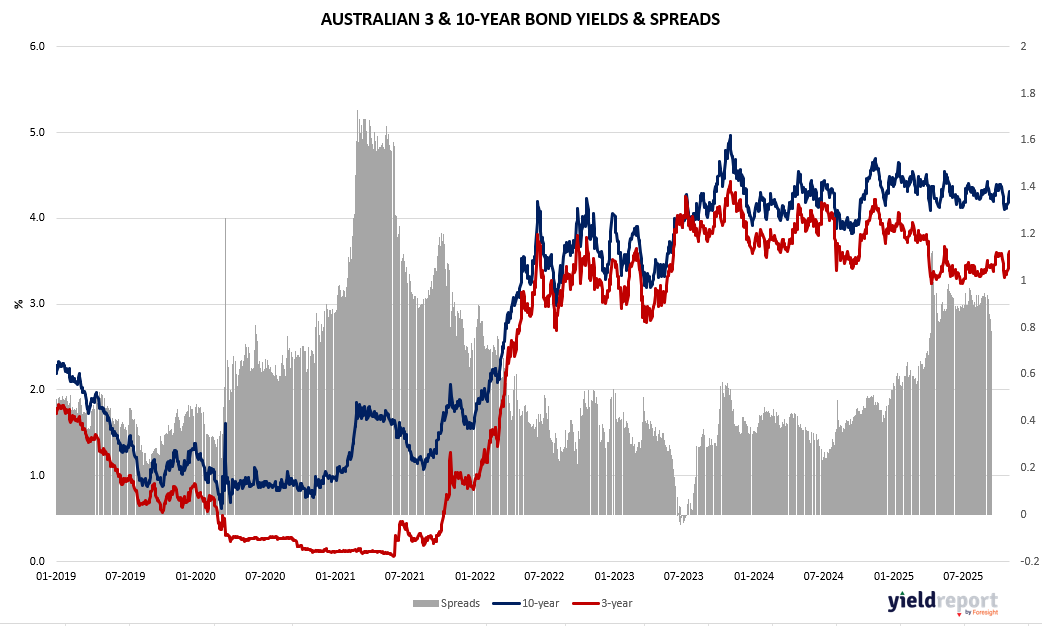

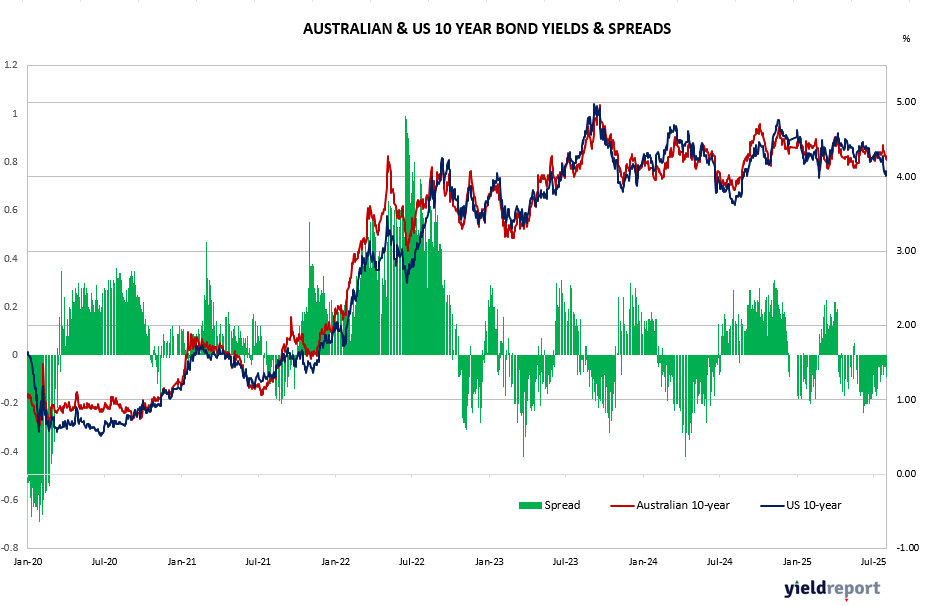

The Australian Bond spreads (3 & 10 years) continue to indicate positive sloping yield curve with significant steepening in the curve occurring from July 2023 (phase 1) and then accelerating from July 2024. The current spread continues to be at cyclical highs although lower than record highs observed in2021. From an investment perspective, steepening yield curves and a rebounding lending environment are likely to boost domestic economic environment and bank profitability. In a similar vein, the spread between the US 2 year bonds and US 10 Year bond has also been steepening since July 2023.

Figure 1: Aust. 3 yr minus 10 yr Bond Spread

Figure 2: Australian & US Bond Yields

Figure 3: US 10-year minus 2-year Bond Spread