| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,562.87 | 40.75 | 0.09% |

| S&P 500 | 6,840.20 | 17.86 | 0.26% |

| Nasdaq | 23,724.96 | 143.81 | 0.61% |

| VIX | 17.69 | 0.25 | 1.43% |

| Gold | 4,007.50 | 11 | 0.28% |

| Oil | 61.11 | 0.13 | 0.21% |

OVERVIEW OF THE US MARKET

Wall Street closed mixed on November 3, 2025, with tech stocks rallying on artificial intelligence deals while broader market breadth remained weak amid conflicting Federal Reserve signals and persistent manufacturing contraction. The S&P 500 rose 0.17% to close at 6,851.97, buoyed by the Magnificent Seven gauge’s 1.2% advance, but its equal-weighted version slipped as over 300 components retreated. The Nasdaq Composite gained 0.46% to 23,834.72, while the Dow Jones Industrial Average fell 0.48% to 47,336.68, dragged by healthcare names like UnitedHealth and Merck. Amazon surged 4% after inking a $38 billion, seven-year deal with OpenAI for Nvidia-powered cloud services, lifting Nvidia 2.2% and fueling AI optimism. Kenvue jumped 12.3% on its $40 billion acquisition by Kimberly-Clark, which sank 14.6%. Other movers included Cipher Mining up 22% and Pfizer little changed.

US factory activity shrank for an eighth straight month in October per ISM data, with easing inflationary pressures, while consumer staples and materials sectors lagged. Fed officials staked out divided positions ahead of the December meeting: Chicago’s Austan Goolsbee voiced inflation concerns and no rush to cut, San Francisco’s Mary Daly urged an open mind on a December move, and Governor Stephen Miran argued policy remains restrictive, heightening downturn risks. Investors eye this week’s ISM non-manufacturing PMI, ADP payrolls, and Challenger layoffs for labor clues amid the government shutdown’s data blackout.

Strategists noted the rally’s concentration, with UBS’s Ulrike Hoffmann-Burchardi highlighting high valuations and murky Fed outlook but seeing room for the bull market to run. Evercore’s Julian Emanuel warned of volatility from record bullishness, while LPL’s Adam Turnquist and Jeff Buchbinder advised not fighting the tape despite non-linear bull markets. Bespoke Investment Group cited historical November gains in strong years, averaging 2.6% when the S&P is up 10% or more through October. Bloomberg Intelligence’s Christopher Cain and Wendy Soong pointed to strong earnings beats but muted stock reactions, rewarding strength but punishing misses twice as hard.

OVERVIEW OF THE AUSTRALIAN MARKET

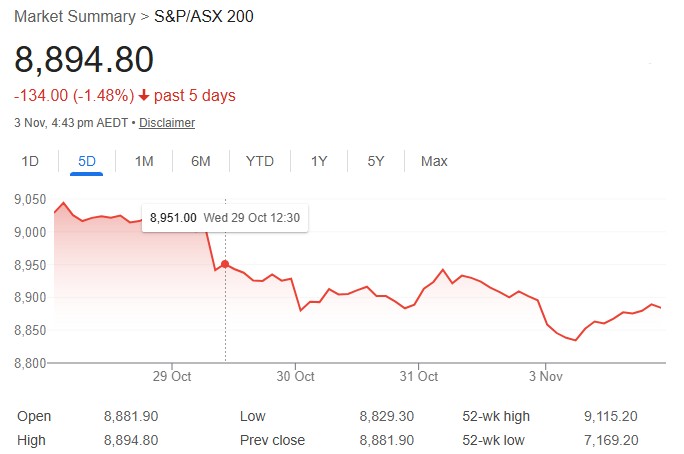

The Australian share market edged higher on November 3, 2025, starting the historically strong month with modest gains as banks and tech offset mining and health care weakness amid softer Chinese data and ahead of the Reserve Bank’s rate decision. The S&P/ASX 200 rose 0.15% to 8,894.8, while the All Ordinaries added 0.05% to 9,182.5, though breadth was poor with decliners outpacing advancers 182 to 98. Information Technology jumped 1.65%, Financials gained 1.25%, and Energy rose 0.79%, but Health Care tumbled 1.68% and Materials fell 0.94%. Westpac climbed 2.8% after full-year results, lifting CBA 2.3%, NAB 0.9%, and ANZ 0.8%. Tech standouts included Megaport up 7.6% and Life360 surging 3.2%.

Resources lagged on iron ore futures dipping to $US105 amid China’s manufacturing contraction, with Pilbara Minerals down 5.2%, Lynas Rare Earths off 8.1%, and Fortescue slipping 1.1%; BHP eased 0.2%. Gold stocks weighed, with the sub-index down 1.4%, though spot gold reclaimed $US4,000/oz. Building approvals surprised higher at 12% month-on-month in September, beating 5% estimates, while S&P Global Manufacturing PMI finalized at 49.7, signaling contraction. Investors await the RBA’s November 4 meeting, expected to hold at 3.6%, with no further 2025 cuts seen by over 90% of economists per Reuters polling after Q3 inflation’s 1.0% core surge.

Capital.com’s Kyle Rodda noted a flat day post-major catalysts, seeking fresh momentum, while CreditorWatch’s Ivan Colhoun said softer September retail supports eventual RBA easing despite inflation pressures. OPEC+’s pause on output hikes lifted oil, aiding Woodside and Santos over 1.1% each. Standouts included Mount Ridley Mines up 75% on CEO appointment and Locksley Resources rising 17.4% on US EXIM Bank support.