| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 47,311.00 | 225.76 | 0.48% |

| S&P 500 | 6,796.29 | 24.74 | 0.37% |

| Nasdaq | 23,499.80 | 151.16 | 0.65% |

| VIX | 18.01 | -0.99 | -5.21% |

| Gold | 3,980.10 | -12.8 | -0.32% |

| Oil | 59.67 | 0.07 | 0.12% |

OVERVIEW OF THE US MARKET

Wall Street closed higher on November 5, 2025, rebounding from the prior session’s sharp drop as dip buyers emerged amid strong services sector expansion and solid earnings, offsetting lingering valuation concerns in tech. The S&P 500 rose 0.37% to 6,796.29, with over 300 components advancing, while the Nasdaq Composite gained 0.65% to 23,499.80 and the Dow Jones Industrial Average added 0.48% to 47,311.00. Communication Services surged 1.63%, Consumer Discretionary up 1.12%, but Information Technology dipped 0.08%, with Nvidia down 1.75%. Rivian jumped 23.36% on narrower loss, Pfizer rose 1.28%, but Snap fell 2.28%. Arm climbed on bullish forecast, AMD rose despite mixed outlook, Super Micro sank on weak sales, and McDonald’s gained 2.2% on US sales beat.

ISM non-manufacturing PMI expanded to 52.4 in October, beating 50.8 poll, signaling fastest growth in eight months despite job losses and high inputs. ADP private payrolls rose 42,000, rebounding from September’s drop. Supreme Court appeared skeptical of Trump’s global tariffs during arguments, potentially forcing $100 billion refunds if invalidated. Investors await balance of trade on November 7, expected at -$61 billion, and PCE prices for inflation clues amid shutdown’s data blackout.

Treasury Secretary Scott Bessent said Sauer presented strong arguments on IEEPA tariff authority. Beijing lifted some retaliatory tariffs on US imports but kept 10% levies post-Liberation Day. Fed’s Miran called ADP rise a welcome surprise but reiterated need for lower rates, with December cut odds at 60%. Edwards Asset Management’s Robert Edwards saw pullback as buying opportunity given earnings growth. Barclays’ Cau expected dips to be bought amid non-extreme positioning and positive seasonality. UBS’s Hoffmann-Burchardi noted consolidation unsurprising but fundamentals intact, with tech P/E lower than dotcom peak.

Strategists from Principal’s Maris eyed US consumer sustainability for 2026 earnings, while Carson’s Detrick cited spectacular season, likely Fed cuts, and benchmark trailing as year-end chase drivers. DataTrek’s Colas remained positive absent macro catalyst, despite fashionable top calls. Apollo’s Zelter warned AI capex rush fueling high valuations and risks.

OVERVIEW OF THE AUSTRALIAN MARKET

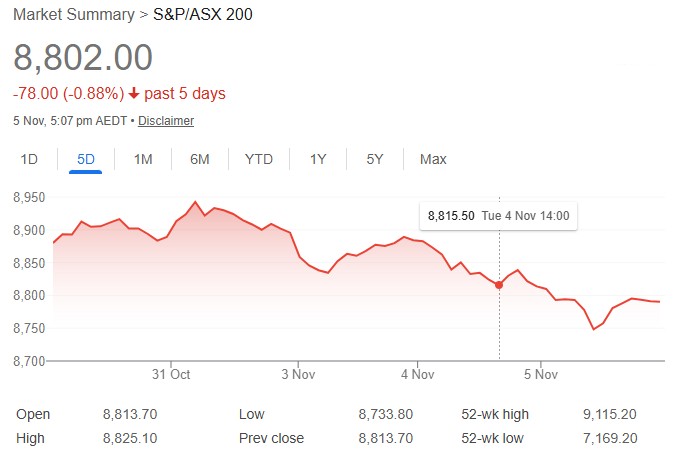

The Australian share market closed modestly lower on November 5, 2025, erasing a late bounce amid economic concerns, softer commodities, and global valuation jitters, though defensive sectors limited losses. The S&P/ASX 200 dipped 0.13% to 8,802.0, while the All Ordinaries fell 0.30% to 9,071.2, with breadth at 86 advancers to 186 decliners. Communication Services rose 0.70%, Utilities gained 0.64%, and Financials up 0.59%, but Information Technology tumbled 1.70% and Materials dropped 1.06%. NAB climbed 1.7% and CBA 1.3% ahead of half-year results, Telstra up 1.4%, but BHP eased 1.0%, Rio Tinto down 0.8%. Gold sub-index fell 1.0% despite spot rebound to $US3,968/oz.

September balance on goods narrowed to A$1.825 billion, missing A$4 billion poll, with exports down 7.8% and imports up 3.2%, signaling trade weakness. Bitcoin teetered near bear market, down over 20% from October high. IG’s Sycamore cited perfect storm of local worries, US rate uncertainty, and post-April rally fatigue.

BTC Markets’ Lucas saw Bitcoin dip as phase shift signal. Standouts included EZZ up 11.7% on dividend, Mayne Pharma gaining 5.9% on FIRB update, but Trigg Minerals down 18.5% on CSAMT findings and Aeris off 17.2% on copper weakness.