| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.664 | 3.631 | 0.033 |

| Australian 10-year bond (%) | 4.373 | 4.322 | 0.051 |

| Australian 30-year bond (%) | 4.999 | 4.967 | 0.032 |

| United States 2-year bond (%) | 3.615 | 3.57 | 0.045 |

| United States 10-year bond (%) | 4.142 | 4.083 | 0.059 |

| United States 30-year bond (%) | 4.7289 | 4.6705 | 0.0584 |

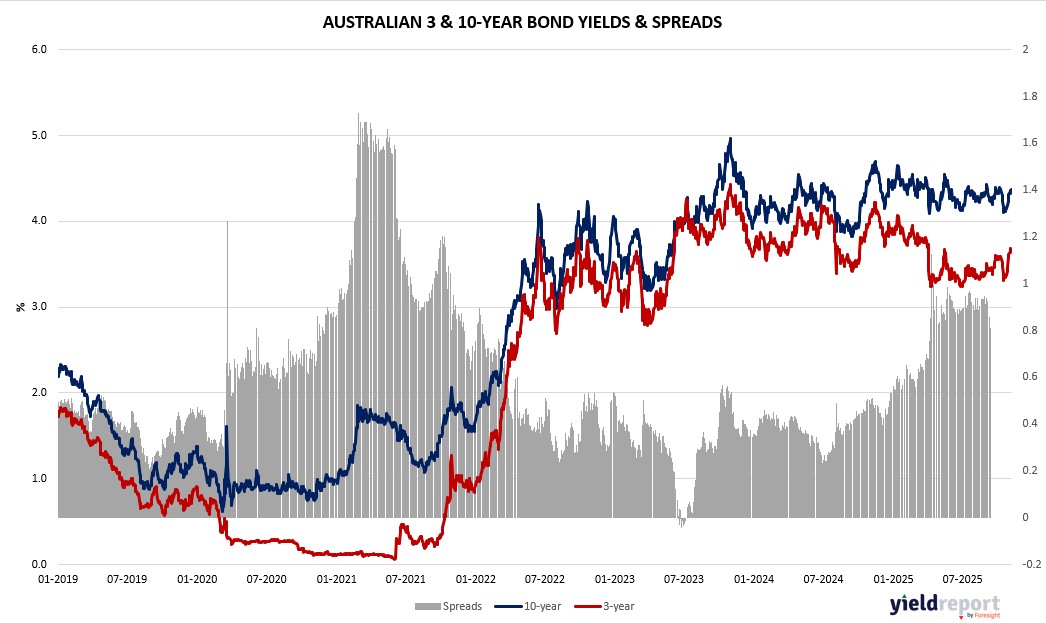

Overview of the Australian Bond Market

Australian government bond yields rose modestly on November 6, 2025, tracking mixed global cues as labor concerns in the US contrasted with resilient local data, while the RBA’s steady stance limited downside. The 10-year yield climbed two basis points to 4.33%, the 2-year edged up fractionally to 3.56%, and the 15-year rose two basis points to 4.65%. Gains reflected rotation into resources equities and commodity strength, with gold and LNG supporting risk appetite, though shutdown-induced US volatility capped moves.

September trade figures showed a surplus of A$3.938 billion, short of the A$4 billion poll but up from prior, fueled by 7.9% export growth including gold surges, offsetting 1.1% import rise. This bolstered views of economic stability, aligning with RBA’s November hold at 3.6%, as per polls. S&P Global PMIs finalized October manufacturing at 49.7 (contraction), services at 53.1, and composite at 52.6, indicating mild expansion but softening demand. Globally, US Challenger layoffs at two-decade highs for October amplified Fed cut bets, pressuring the dollar and aiding AUD stability at 0.651.

Tariff truce extensions discussed by US Treasury’s Bessent, potentially adding 90 days with China, eased inflation fears down under, given export ties. Drug deals with Lilly and Novo for lower prices echoed policy efforts to curb costs, indirectly supporting consumer sentiment. However, shutdown delays in US data like payrolls and GDP cloud Fed paths, with markets pricing a 60% December cut chance, influencing RBA monitoring.

Strategists at Brown Brothers Harriman see US easing worsening labor fragility, while UBS forecasts two Fed cuts by early 2026, favoring fixed-income hedges. Locally, fund flows from high P/E tech and consumer stocks to low P/E miners suggest diversification, with Moody’s Mark Zandi noting resale housing competition amid job angst. Dealers expect steady US auction sizes, but Australian yields may face upside if growth exceeds forecasts. The curve’s modest steepening reflects caution, with oil steady and gold firm, as investors await clarity on tariffs and AI impacts.

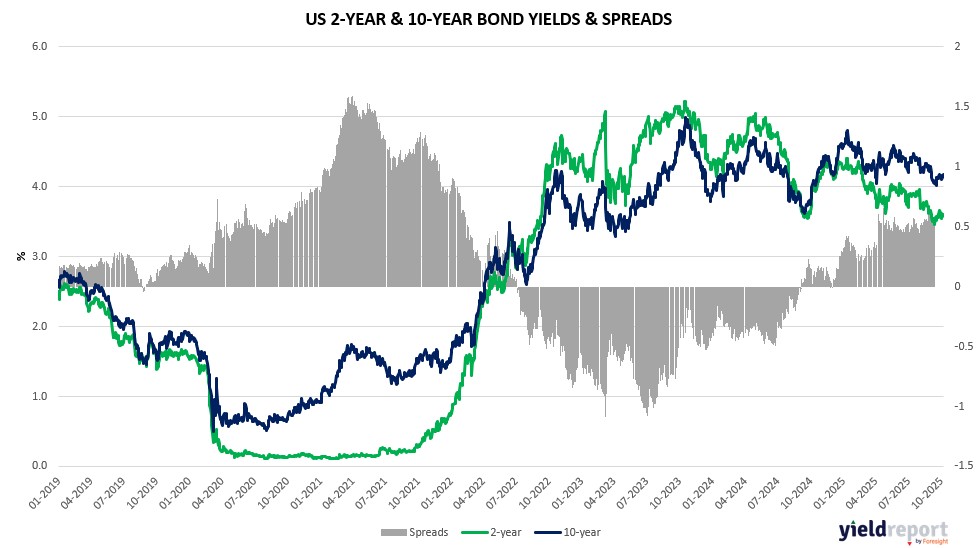

Overview of the US Bond Market

Treasury yields fell across the curve on November 6, 2025, as labor market weakness boosted bets on Federal Reserve rate cuts, countering recent hawkish tones from policymakers. The benchmark 10-year yield dropped seven basis points to 4.09%, its steepest decline in about a month, while the 2-year yield slid seven basis points to 3.56% and the 30-year fell six basis points to 4.68%. The move reflected a flight to safety amid equity volatility and private data signaling a fragile jobs backdrop, with money markets pricing over a 60% chance of a December cut, up from prior levels.

The government shutdown’s data blackout has shifted focus to alternative sources, amplifying their impact. Challenger’s report of October layoffs surging to 153,074—the most since 2003—highlighted AI-driven disruptions and cost-cutting, echoing 2022 tech layoffs but with broader risks in a low-hiring environment. Revelio Labs’ 9,100 job loss figure added to doubts about labor reacceleration, pressuring the Fed to act despite inflation at 3% in September, above the 2% target. Fed speakers like Chicago’s Austan Goolsbee expressed unease over missing data, while Cleveland’s Beth Hammack prioritized inflation risks, yet markets leaned dovish.

Bond gains were supported by tariff developments, with Treasury Secretary Scott Bessent noting ongoing US-China talks on extending the truce, potentially adding 90 days, which could ease inflationary pressures. Drug price agreements with Lilly and Novo, offering tariff relief for lower Medicare costs, also signaled policy efforts to curb living expenses amid voter concerns. However, the shutdown’s extension risks further delays in key data like nonfarm payrolls and GDP, clouding the outlook.

Strategists at Brown Brothers Harriman stuck to expectations of a 25 basis-point December cut, citing restrictive policy’s potential to worsen employment fragility. UBS’s Ulrike Hoffmann-Burchardi forecasted two more cuts by early 2026, viewing quality fixed-income as appealing for income and slowdown hedges. JPMorgan’s client survey showed net long positions shrinking to two-month lows ahead of potential Fed dissent, while asset managers pared longs in futures. Dealers anticipate steady coupon auction sizes for August-October, aligning with April guidance. The Bloomberg Dollar Spot Index fell 0.3%, aiding the rally, as investors diversify amid high equity valuations and AI uncertainties, with oil steady and gold little changed.