| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 46,912.30 | -398.7 | -0.84% |

| S&P 500 | 6,720.32 | -75.97 | -1.12% |

| Nasdaq | 23,053.99 | -445.8 | -1.90% |

| VIX | 19.68 | 0.18 | 0.92% |

| Gold | 4,019.00 | 28 | 0.70% |

| Oil | 60.19 | 0.76 | 1.28% |

OVERVIEW OF THE US MARKET

Wall Street staged a late rebound on November 7, 2025, amid optimism over progress in ending the US government shutdown, though tech weakness capped gains and led to the Nasdaq’s worst week since April. The S&P 500 rose 0.1% to 6,728.80, recovering from a 1.3% intraday drop after Senate Democrats proposed scaling back demands, signaling potential compromise despite Republican rejection. The Dow Jones Industrial Average added 0.2% to 46,987.10, while the Nasdaq Composite slipped 0.2% to 23,004.54, down 3% for the week as AI doubts intensified. Nvidia edged up 0.04% but megacaps like those in the Magnificent 7 fell 0.9%, with the Nasdaq 100 posting its steepest weekly loss since April amid valuation concerns.

Consumer sentiment plunged to near-record lows per the University of Michigan’s index at 50.3, battered by shutdown impacts and high prices, heightening labor market fears. With official payrolls delayed, private data loomed large: 22V Research highlighted labor unwind as the top trading risk, while recent Challenger and Revelio reports showed surging layoffs and net job losses, fueling bets on Fed easing. Markets priced a 65% chance of a December cut, up slightly, though Fed speakers like BlackRock’s Rick Rieder urged rates to 3% amid softening jobs.

Corporate news mixed: KKR fell on a fee charge despite record earnings, Sweetgreen cut guidance amid weak demand, sinking shares, while Wendy’s beat on sales resilience. Airlines pared gains but rose overall—American up 3.8%, Delta 1.9%—on shutdown deal hopes, though Transportation Secretary Sean Duffy warned of 20% flight cuts if unresolved. Crypto rebounded, Bitcoin up 2.3% to $103,422, trimming weekly losses after a $300 billion selloff.

Broader sentiment reflected froth purge, per Nationwide’s Mark Hackett, with BMO’s Ian Lyngen noting data distortions lingering post-shutdown. TD Securities eyed Thanksgiving travel as a backstop, while Wolfe’s Chris Senyek warned of market risks if Fed skips December amid negative payroll surprises. Piper Sandler’s Craig Johnson saw supportive flows despite anxiety, and Goldman’s Tony Pasquariello viewed the dip as temporary in a bull trend. Investors eye next week’s earnings like Disney and Cisco, plus Nvidia’s pivotal report, as S&P earnings beats hit 82.5%, but labor fragility could cap upside.

OVERVIEW OF THE AUSTRALIAN MARKET

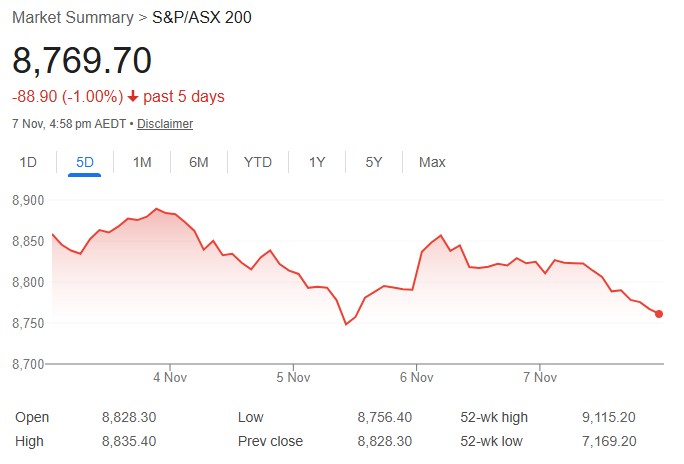

The Australian share market closed lower on November 7, 2025, extending weekly losses to its lowest in over three months amid rate-sensitive weakness and global tech jitters. The S&P/ASX 200 fell 0.7% to 8,769.7, down 1.3% for the week and 3% over two weeks, while the All Ordinaries dropped 0.7% to 9,031.7. Early gains faded as financials tumbled 1.3%, with Macquarie Group down 5.7% on earnings miss, and big banks mixed—Westpac and CBA lower, NAB up modestly. CVS Lane’s Fiona Clark noted sparse highlights amid grim outlook.

Sectors showed defensives outperforming: Communication Services up 0.7%, Consumer Staples 0.6%, Energy 0.5%, Real Estate 0.5%, Utilities 0.2%, Health Care flat. High P/E areas lagged: Information Technology down 2.3%, Consumer Discretionary 1.1%, Financials 1.3%, Industrials 0.9%. Materials slipped 0.5% as iron ore futures below US$103/tonne on China export drop, despite rare earths rebound; BHP, Rio, Fortescue lower. Gold miners mixed as spot topped US$4,000/oz.

Top performers: AUB Group up 6.3% on EQT proposal, Sun Silver 8.9% on antimony discovery. Laggards: Alliance Aviation down 42.7% on guidance cut, Block 15.8% on US earnings miss echoing Nasdaq woes, Qantas 6.6% on soft revenue guidance, Zip Co. 6.6% on funding update, OOH!Media 6% on trading weakness.September trade surplus at A$3.938 billion missed polls but export growth at 7.9% supported resilience, per RBA’s steady 3.6% rate. AUD/USD held 0.648 amid risk-off, correlated to S&P 500’s 3.7% from highs. Uranium plays fell amid sector weakness.

CVS Lane highlighted rates grimness pressuring leveraged sectors. Investors eye AGMs for Coles, Goodman, and earnings from ANZ, Orica. HSBC, Morgan Stanley, UBS maintain bullish on earnings/AI, but shutdown/AI doubts temper. Bitcoin up modestly but in bear market, down 23% from peaks.