Global financial markets exert a profound influence on Australia’s financial conditions. In her recent speech at the Australian Securitisation Conference, Penelope Smith, Head of the RBA’s International Department, explored how international developments—from monetary policy shifts to geopolitical tensions—transmit into Australia’s economy. This article provides a comprehensive analysis of those dynamics, structured into key sections, and indicates where charts should be placed for visual clarity.

Global Policy Rate Trends

Over the past year, major central banks have adjusted their policy stances in response to moderating inflation and evolving economic conditions. The U.S. Federal Reserve, after a series of hikes, began easing rates in 2024 and continued into 2025, signalling confidence that inflationary pressures were under control. Similarly, the European Central Bank reduced its policy rate, while Japan stood out as an exception, implementing modest tightening measures. These shifts have significant implications for global liquidity and borrowing costs. Lower global rates generally ease financial conditions worldwide, influencing Australia’s neutral interest rate and capital flows. For Australia, this means that even without domestic policy changes, global monetary easing can create a more accommodative environment, affecting investment decisions and household borrowing costs. The interplay between global and domestic rates underscores the importance of monitoring international developments closely.

Exhibit 1: Comparative Policy Rate (2024–2025)

Central Bank Balance Sheet Reduction

In addition to interest rate adjustments, central banks have been actively managing their balance sheets. The Federal Reserve, for instance, continued its quantitative tightening program, reducing its holdings of government securities and mortgage-backed assets. This runoff is expected to conclude once reserves reach an ample level, likely by the end of 2025. The European Central Bank and Bank of Japan have also scaled back their asset purchase programs, albeit at different paces. These actions influence global liquidity conditions and can affect funding costs for banks and corporations.

For Australia, reduced global liquidity may lead to tighter credit conditions, particularly for institutions reliant on offshore funding. Understanding these dynamics is crucial for anticipating potential spill-overs into domestic markets.

USD vs Treasury Yields Post-Tariff

Geopolitical developments, such as tariff announcements, have triggered notable market reactions. Following the U.S. administration’s decision to impose new tariffs in April 2025, the U.S. dollar unexpectedly depreciated, while Treasury yields spiked. This divergence reflects investor concerns about fiscal sustainability and inflationary pressures rather than confidence in the dollar’s safe-haven status. For Australia, movements in the USD are particularly relevant because they influence the AUD exchange rate. A weaker USD often leads to AUD appreciation, which can tighten domestic financial conditions by making exports less competitive and imports cheaper. These currency dynamics serve as an important transmission channel for global shocks.

Equity Performance & Corporate Spreads

Despite heightened uncertainty, global equity markets have performed strongly in 2025, buoyed by optimism surrounding artificial intelligence and supportive fiscal policies. Corporate bond spreads have remained tight, indicating robust investor risk appetite. However, valuations appear stretched, raising concerns about potential corrections. For Australia, global equity rallies can have mixed effects: while they may boost wealth through superannuation funds, they also tend to strengthen the AUD, offsetting some of the positive impact on financial conditions. Moreover, tight corporate spreads globally can influence pricing in Australian credit markets, albeit to a lesser extent given the dominance of bank lending domestically.

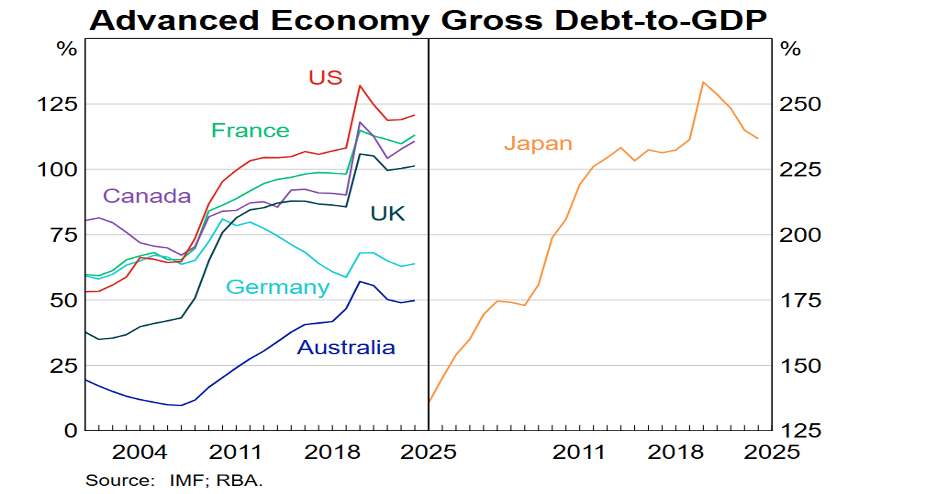

Government Debt-to-GDP Ratios

Fiscal pressures have intensified globally, with government debt levels rising due to pandemic-related spending, ageing populations, and increased investment in climate adaptation and defense. In the U.S., debt-to-GDP ratios have surpassed 130%, while Japan’s levels remain above 250%. Such elevated debt burdens contribute to higher long-term yields and term premia, as investors demand compensation for perceived risks. For Australia, these global trends can influence domestic bond markets, raising borrowing costs for governments and corporations. The link between global fiscal dynamics and local financial conditions highlights the interconnected nature of modern economies.

Exhibit 2: Government Debt-to-GDP Ratios Across Key Economies

Gold Price Surge

Gold has emerged as a standout performer in 2025, with prices surging by over 50% year-to-date—the fastest annual increase since 1979. This rally reflects a combination of factors: geopolitical tensions, diversification by emerging market central banks, and speculative demand from retail investors. For Australia, a major gold exporter, rising prices can support export revenues and improve terms of trade. However, the broader implications for financial conditions are nuanced, as gold’s performance often signals underlying risk aversion in global markets.

Exhibit 3: Emerging Gold Price

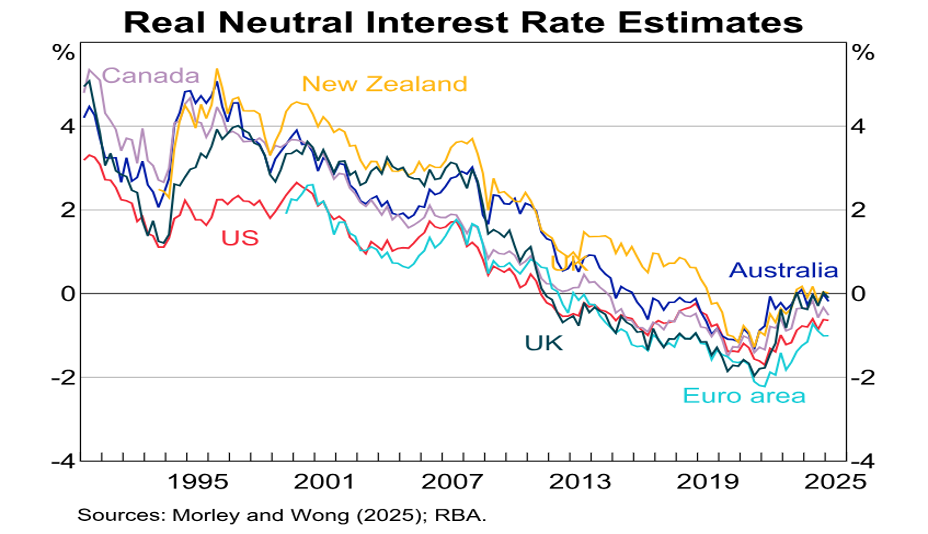

Neutral Real Interest Rate Decline

One of the most significant structural trends influencing financial conditions is the decline in neutral real interest rates across advanced economies. Driven by demographic shifts, subdued productivity growth, and strong demand for safe assets, these rates have fallen steadily over the past decade. Post-pandemic, estimates remain uncertain, with some models suggesting a modest rebound due to fiscal expansion and technological innovation. For Australia, research indicates that roughly half of the variability in its neutral rate stems from foreign shocks, particularly movements in the U.S. neutral rate. This finding underscores the importance of global factors in shaping domestic monetary policy settings.

Exhibit 4: Declining Neutral Real Interest Rates (2010–2025)

Correlation of Risk Premia

Risk and term premia in Australia exhibit a high degree of correlation with those in other advanced economies. When global equity risk premia rise or corporate spreads widen, similar patterns often emerge domestically. However, Australia’s financial system—dominated by variable-rate bank lending—moderates the direct impact of these shifts compared to economies with more market-based financing. Additionally, the prevalence of superannuation means that household consumption is less sensitive to short-term equity market fluctuations. These structural features provide resilience but do not eliminate the influence of global financial conditions.

Conclusion

Australia’s financial conditions are shaped by a complex interplay of global monetary policy, fiscal dynamics, risk sentiment, and structural trends. While the domestic banking system and exchange rate provide buffers against external shocks, the Reserve Bank of Australia must remain vigilant to international developments—particularly those originating in the United States. Understanding these transmission channels is essential for effective monetary policy and financial stability in an increasingly interconnected world.