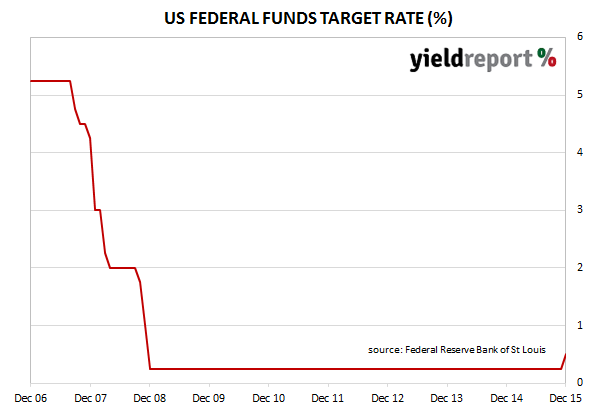

In what could be described as one of the most telegraphed changes in US interest rate policy, the US Federal Open Markets Committee (FOMC) announced it was changing the federal funds rate from 0.25% to 0.50%. Markets had been expecting this “lift off” for some time and the odds of such a rise were at around 80% after recent US inflation data was released. US 2 year and 10 year treasury yields spiked after the meeting but quickly settled back and were only modestly up over the day, finishing at 1.00% and 2.27% respectively.

This time there were no dissenters; Federal Reserve Bank of Richmond President Jeffrey Lacker had voted for rate increases at the September and October FOMC meetings. Other members had voted to keep rates steady but votes were unanimously in favour of raising the target rate in this latest meeting.

The FOMC pointed to the “solid rates” at which household spending and business investment had been increasing and how a range of labour market indicators had shown “further improvement”. However, the committee statement also noted net exports had been “soft” and inflation was below the 2% longer run target. Imports volumes had risen as a result of a stronger currency, thus replacing US produced goods and services while energy (oil) and import prices had fallen, lowering inflation measurements.