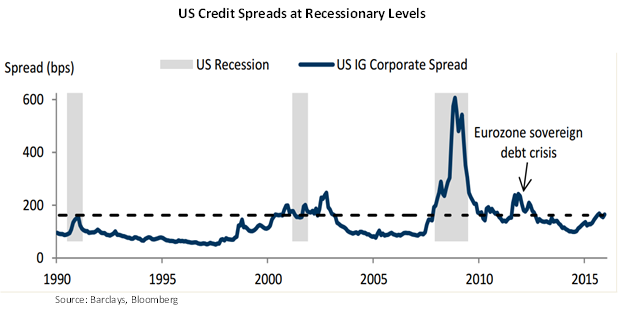

The US high yield bond market returned -4.6% in 2015, the worst in the history of the asset class outside of a recession. According to Goldman Sachs, current investment grade spreads are at recessionary levels and this has nervous investors asking the question – is the US heading for a recession? Or, is the market simply pricing in the likelihood of the Fed raising interest rates in 2016?

A US recession doesn’t look likely with employment growth looking strong. So another explanation is perhaps the culprit. Certainly corporate bond issuance in the US has been massive with companies taking advantage of low rates, willing investors and banks happy to sell the paper. Much of those funds raised have funded share buy-backs and driven up EPS rather than grow the underlying business. And while this has been good for CEO’s remuneration, markets are asking what happens when debt servicing costs increase or repayment of debt is required. Will these same companies be able to refinance these deals at competitive rates? This has likely led to a deeper analysis of credit risks and a stratification of the higher yield bond markets. It looks to us like a market where credit analysts will earn their money.