Evans & Partners recently issued a note looking at Ramsay Healthcare “CARES”, which are “step-up” hybrid securities trading on the ASX. As with other hybrids, step-ups have a face value, typically $100, and pay a percentage of the face value as income. The term “step-up” refers to a penalty rate of interest which is added to the ordinary interest if a step-up hybrid is not redeemed on the step-up date.

In the case of the Ramsay step-ups, the step-up date was 20 October 2010 and because Ramsay did not redeem the securities on that date, an additional 2% was added to the interest/distribution. From that point on, the interest calculation formula* became BBSW + 2.85% (ordinary margin) + 2.00% (step-up penalty). This amount includes franking. The running yield of over 7.00% (including franking credits) may be tempting on the face of it but the terms of the hybrid contain a clause that represents a risk to investors. This clause allows Ramsay Health Care to redeem the hybrids on any dividend date.

As Evans and Partners point out, if an investor paid more than face value ($100) for these hybrids on the basis of the an attractive income stream and the company then decides to redeem the hybrids at face value, the investment proposition may well be a loss-making one.

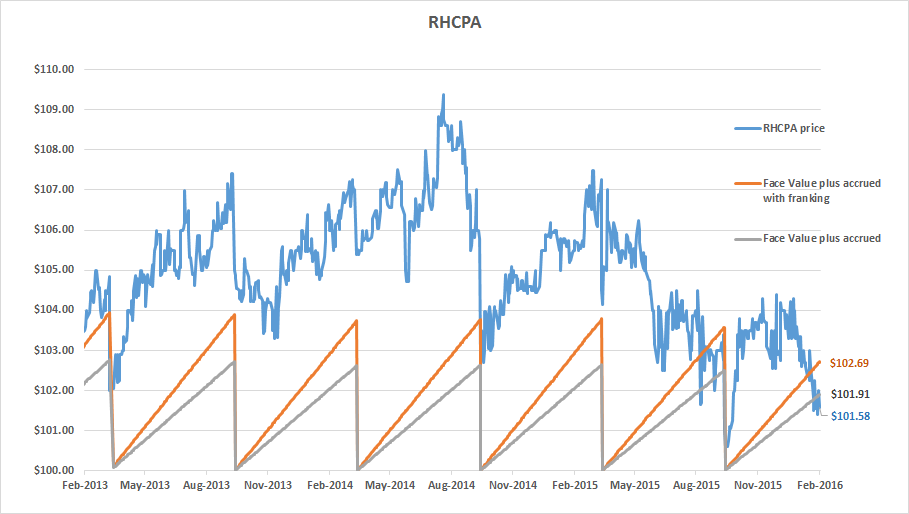

A glance at the chart below shows that the hybrids have traded over the $100 face value for all of the past 3 years. This is largely based on the generous income stream. But it ignores the risk that the company may one day redeem the securities at face value incurring an immediate capital loss on the hybrids.