Investors often YieldReport ask, “What are the best hybrids to invest in?” YieldReport as an independent news source does not make explicit recommendations but it does monitor broker recommendations and report on those from time to time. Hybrids, of course, are relatively complex instruments and investors need to be fully aware of the characteristics of each one and conduct diligence beyond a broker recommendation before committing hard-earned capital.

One recommendation seen from time to time is for investors to buy NAB Income Securities. The recommendation is generally based on the fact the income is reasonable, NAB is secure and NAB are likely to redeem the securities at face value at some point. The suggestion has also been made the securities are not Basel III compliant and thus will not eventually qualify as Tier 1 capital; hence NAB will be motivated to redeem them.

A closer look at the securities (ASX Code: NABHA) shows they are perpetual income securities issued by NAB and pay a distribution rate of 1.25% plus the 90 day bank bill rate each quarter (currently around 3.55% pa in total). There is no franking. The securities were issued in 1999 and rank ahead of ordinary equity in the event of a company wind-up. They are not a regular bond and in fact behave quite differently. Unlike many of the recently issued hybrids, the company can redeem them at any time at their face value of $100 but there is no mandatory conversion date. They, in fact, may never be repaid. Under the terms, the company can suspend the payment of distributions but if it does, it cannot pay the dividend on its ordinary shares. This is, in part, an incentive for NAB to keep paying distributions on the income securities.

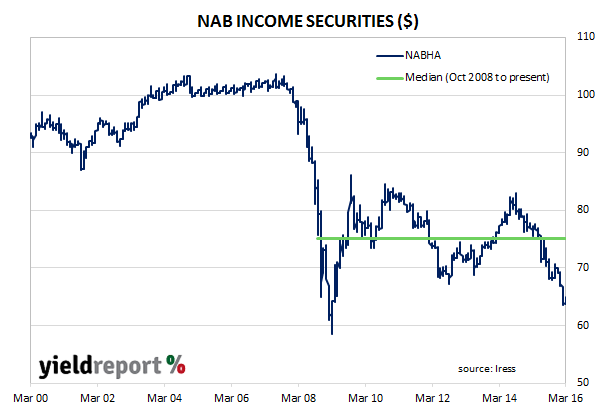

A look at the chart below shows how this ‘recommendation’ of has fared. Several things seem obvious:

- Investors in the initial issue price at $100 have not fared well.

- Investors buying in the secondary market have not fared well.

- Almost all investors in NABHA have not fared well except for those which swam against the tide and purchased in the period around March 2009. They, at least, still have a modest capital gain as well as some income along the way.

The securities are now priced at around $65 giving a running yield (income divided by purchase price) of around 5.50% which is less than many of the other hybrids on the market. The securities have weakened considerably in price in the past 2 years and the reasons are not necessarily clear cut. Some investors may be tired of holding a security which is falling in price and others may simply be selling to crystallise a loss and invest in other higher yielding securities. NAB has made no comments in relation to redeeming the securities. Regardless, it is another timely reminder of the complexities involved with hybrid securities and how investors and advisers need to be well informed of the characteristics of each hybrid, lest they suffer the same fate as NABHA holders.