Seven Group announced their annual profit results and at the same time announced an on-market buy-back of up to 10% of the hybrid TELYS4 (ASX code: SVWPA) on issue. Richard Richards, Seven’s chief financial officer said the company would buy the preference shares if the price fell below a level it thought was reasonable. “Today we announce the extension of recent capital management initiatives with the buy-back of up to 10 per cent of the TELYS4 shares on issue, allowing value to be captured should its price fall below what we believe to be its intrinsic value.” Interestingly they didn’t say what that intrinsic value was so investors might well assume in the absence of any buying that the firm thinks the TELYS4 are overvalued.

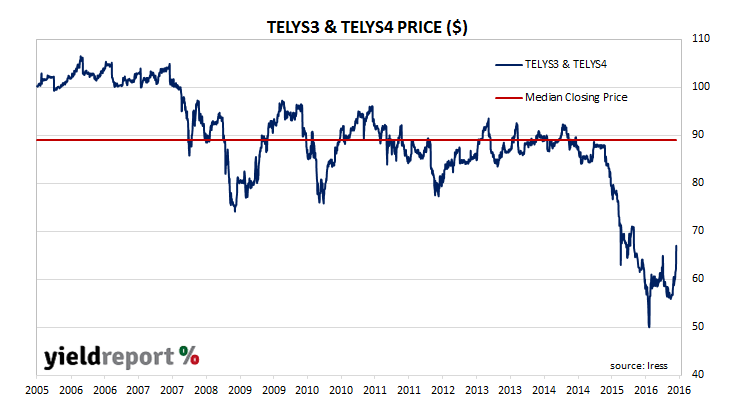

TELYS3 (ASX code: SEVPC) were first issued in 2005 at $100 and the securities paid a fully franked floating rate dividend where the grossed up an amount equal to BBSW + 250bps. In 2010 when Seven Network and Kerry Stokes’ Westrac Holdings businesses were put together, holders of the TELYS3 were offered replacement securities in the form of TELYS4. The floating rate dividend was “stepped-up” by 225bps so holders would receive the equivalent to BBSW + 475bps.

The price of the securities has plunged in recent times, sending the gross running yield well above 15%. Being a perpetual security there is little to anchor the price to or near the securities’ $100 face value but Seven’s buy-back announcement has since triggered investor interest and the price has partially recovered. Even so, the yield is still substantially in double-digit territory. Another possible attraction is the potential for Seven to establish a quasi-floor price through their on-market purchases. Any on-market purchases will need to be reported to the ASX, giving investors some idea of the price Seven is prepared to pay.