ANZ Converting Preference Shares Series 2 have a December 2016 mandatory conversion date. They were first issued in November 2009.

Under the Basel 3 capital requirements it was anticipated that ANZ would have to replace the original hybrid security and markets had been expecting an announcement close to December. ANZ has ‘gone early’ and announced it intends to issue ANZ Capital Notes 4 (ASX code: ANZPG), seeking to raise at least $1 billion (subject to demand). The new capital notes will qualify as Additional Tier 1 (AT1) capital under the Basel III bank regulatory framework, which means they have the now-standard “trigger events” which may lead to early conversion into ordinary shares or write-off. At the prevailing level of interest rates, they will pay around 6.45% inclusive of franking credits over the first quarterly period.

The new capital notes have an indicative distribution of BBSW plus a margin of 470bps to 490bps. The final margin will be determined by a book build, which is a tender process managed by investment banks on behalf of ANZ. The first call date, the date at which ANZ can exchange the securities is on 20 March, 2024 and, by convention, securities are typically redeemed on this date. Exchange, in the context of listed hybrids, can mean redeem, resell to a third party or convert into ordinary shares. The scheduled maturity date is on 20 March 2026.

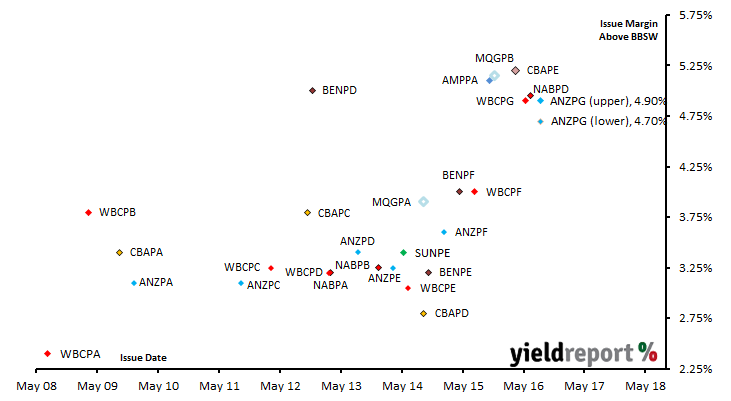

The chart below shows the history of issue margins of hybrid securities over the last eight years, including the GFC period in 2008/2009. The new capital notes are shown at both the lower end of the indicative margin (470bps) and the upper end (490bps). Issue margins are set close to the margins of comparable hybrids already trading on the ASX and as margins of existing hybrids have fallen, the new ANZ hybrids will have a lower issue margin than the Westpac, NAB or CBA hybrids which preceded them. However, they are still fairly high from a historical point of view.

Perhaps what is more important to the market than the issue margin of other comparable securities is where the new hybrids fit relative to current trading margins available to investors. Prices for securities change as soon as trading begins, whether it is on an organised market such as the ASX or on an over-the-counter (OTC) market. Other securities issued at lower margins may have fallen in price, which generally means their trading margin will have risen. The chart below shows the trading margins of comparable securities which trade on the ASX as at the close of business 17 August 2016, as well as the new hybrids at both the lower and upper ends of the indicative margin range.