In the lead up to the release of the September quarter CPI figures, much of the public discussion has been about how weak CPI figures would need to be in order to put a rate cut back into contention at the RBA November meeting. Recently, the RBA had referred to the September quarter CPI figures as worthy of our attention and, so while CPI figures are usually given considerable weighting compared to other economic data, the level of scrutiny and anticipation was up a notch this time.

The figures have now been released by the ABS and, although headline figures were stronger than the market expected, seasonally-adjusted and core numbers generally were viewed by economists as being on the low side. Seasonally-adjusted consumer inflation was 0.4% for the quarter and 1.4% for the year to September which is basically in line with market forecasts.

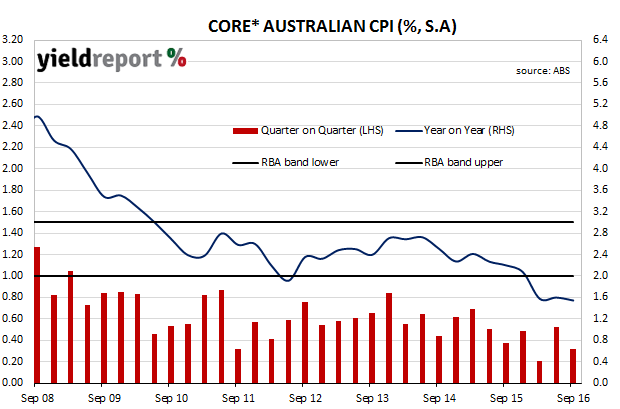

“Core” inflation measures favoured by the RBA, such as the “trimmed mean” and the “weighted median” were slightly below consensus when considered together. For the quarter, the trimmed-mean measure increased by 0.4% while the weighted-median increased by 0.3% and the average of the two annual rates came in at 1.5%.

Before the announcement, cash contracts had implied a 16% probability of a November rate cut but, after the announcement, the probability slipped to 4%. February contracts behaved in a similar fashion. 10 year bond yields rose 2bps on the news but finished the day down 1bp at 2.245% while 3 year bonds closed 3bps higher at 1.72%. The AUD jumped from 76.40 US cents to over 77 US cents before it settled back at around 76.80 US cents. All of this indicates financial markets viewed the numbers as supportive of higher interest rates.

*Average of trimmed-mean and weighted-median measures