Although some economists thought November’s RBA meeting was “live”, most pundits gave little weight to such an outcome. Just as well, because the RBA announced this week it had chosen to keep the cash rate at 1.50%.

Reactions in bond and currency markets were subdued but both hinted of an expectation by participants of higher rates in the future. The AUD rose 0.4 US cents on the day and the 10 year bond rate implied by futures contracts rose from 2.325% to 2.360%.

Westpac chief economist Bill Evans said the statement accompanying the decision confirmed his view Australia’s inflation outlook “is unlikely to be the source of any future policy adjustment.” That is, unless inflation is unexpectedly and abnormally low, the RBA will not cut rates again in this cycle on the basis of inflation figures. Then again, he is not totally against the possibility of a rate cut. “However, with inflation only likely to track along the bottom of the 2-3% target band next year there will be scope to ease further should growth, and the labour market in particular, profoundly disappoint.” He also concedes if there were any movement from the RBA next year, “it will be down rather than up in 2017.”

Close of business, 1 November 2016

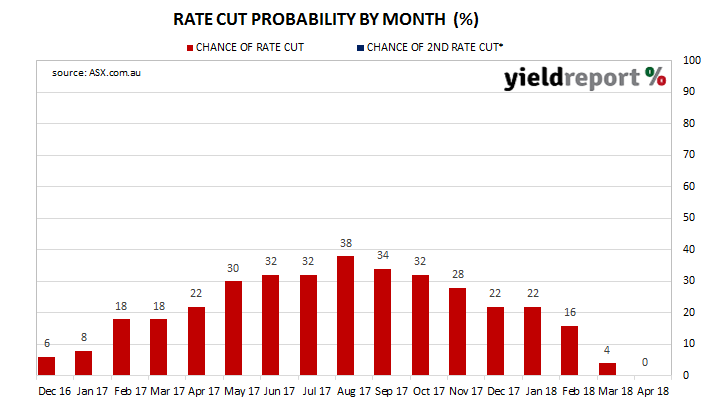

The focus now moves to February’s meeting, which is the next meeting after December quarter statistics such as CPI and employment figures are released. One of the interesting developments since October’s meeting has been the ratcheting back of expectations for a rate cut as implied by cash contracts. At the end of Melbourne Cup Day, not only were contracts implying buyers and sellers placed less than a 50% chance of a rate cut in 2017, they are close to implying a rate rise in 2018. Not yet, however, and as we have seen over the last twelve months, expectations can change rapidly.