By guest contributor Michael Boye from Saxo Bank

Following the initial shock reaction and contrary to the preceding message from various doomsayers, the new Trump administration has been received overwhelmingly positively by financial markets so far.

The president-elect has introduced a far more conciliatory tone, which began from the very first acceptance speech and which has replaced the irreconcilable rhetoric from the campaign trail. As a result, investors are seemingly now already discounting his promises of a growth agenda, including tax cuts, new infrastructure investments and financial deregulation, at near face value.

This combination of stronger growth confidence and rising inflation expectations on the back of debt-financed fiscal stimulus has seen developed markets’ government bond yields surge dramatically in response.

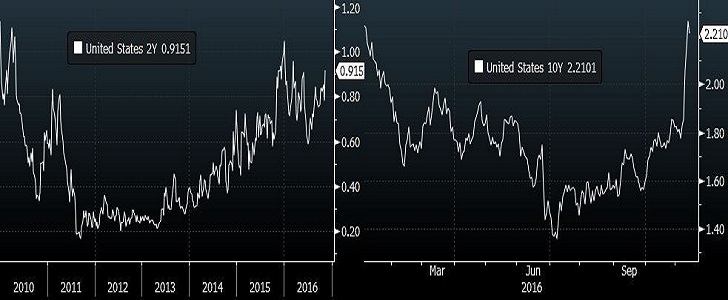

In the US, Treasury yields are traded close to the year-high levels, which was last seen back in January. Government yields have risen across the curve with 10-year yields now at 2.22% and 30-year yields traded briefly above the 3% mark.

In the shorter end of the yield curve, 2-year yields, which is a better indication of the short-term policy direction of the Federal Reserve, broke above the 1% mark – a milestone that it hasn’t traded at or above consistently for several years.

As for the Federal Reserve, it is now priced at an almost definitive 92% chance to hike its benchmark interest rate at the December policy meeting, a stunning comeback from from the sub-40% chance traders were giving this scenario during the early hours right after the upset election result.

US government yields have surged after the election of Donald Trump as the next president

Even though a case could be made for higher interest rates in the longer term under a Trump administration, this recent and rapid development is quite remarkable even given the current argument justifying the move.

As the fiscal expansion is likely to be financed by bigger budget deficits, the Federal Reserve might still want to pursue a financial repression policy, in which interest rates are kept artificially low in order to keep borrowing costs down. This would especially be the case if it becomes less independent – as has been the widespread concern under the new president.