By guest contributor Michael Boye from Saxo Bank

The threat of dramatically increasing interest rates primarily in the US has been latent for years, but for one sector its reality has serious repercussions – emerging markets, where USD denominated debt still constitutes a significant share of both corporate and government financing.

Emerging market bonds have long been driven by two major supportive long-term forces; namely improving economic and market fundamentals as well as record low (and in some cases negative) yields across the developed world.

It has forced global investors to focus on (higher) yielding alternatives. Now that US interest rates are widely expected to rise, the narrative is that this debt would obviously become much more difficult to service.

Furthermore, investors have been worried that if the rise in yields were to puncture the global economic recovery, the commodity-dependent developing nations be first in line to feel the pressure, along with potential turmoil in financial markets globally, which could add insult to injury as investors flee the region and withdraw investments.

Just when you thought the outlook couldn’t be more gloomy, Donald Trump was elected as the next president of the United States. Among his promises (or threats depending on your perspective) is the protectionist anti-free trade agenda which aims to take back jobs from the emerging economies.

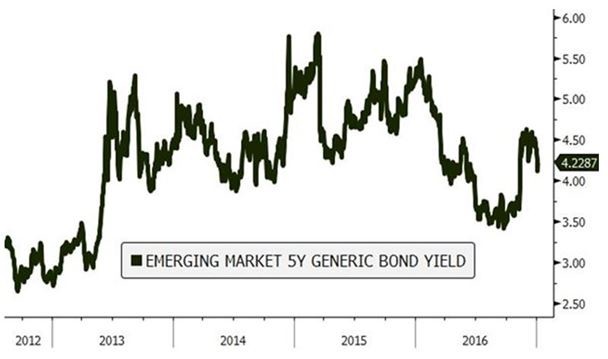

Emerging Market 5-year generic bond yield. Computed as the 5-year generic US treasury yield with addition of the Markit CDX Emerging Markets Index spread.

Source: Saxo Bank and Bloomberg

The election did cause the market to sell off late in 2016, when in November investor cash inflow to emerging market bond funds regressed for the first time four months. However, so far this year, while the theme of rising interest rates has persisted in both the US and Europe, these bond markets have performed surprisingly solidly.