NAB released its quarterly report this week and, tucked away was one sentence which flagged the bank’s intention to issue a new Tier 2 note. “As part of NAB’s ongoing commitment to maintain a strong and efficient capital position, NAB is considering issuance of a new ASX-listed Subordinated Tier 2 Capital security, subject to market conditions, including any competing supply.” Tier 2 securities were previously referred to as debt instruments; they include bonds and notes. In these days of conversion clauses and write-off clauses, the distinction between debt and equity is blurred and so securities which have more debt-like characteristics are referred to as Tier 2 securities, while securities which have more equity-type characteristics are classified as Tier 1 securities.

NAB has now announced its intention to issue $750 million worth of subordinated Notes (ASX code: NABPE), with the ability to raise more or less than this amount. The proceeds will be used to repay NAB Subordinated Note I (ASX code: NABHB) holders, as well as for general purposes.

The new capital notes will qualify as Tier 2 capital under the Basel III bank regulatory framework, which means they have the now-standard “non-viability trigger event” clauses which may lead to early conversion into ordinary shares or a write-off of the notes if conversion does not occur. At the prevailing level of interest rates, they will pay around 4.0% (annualised). As interest rates change, specifically the bank bill swap rate, quarterly payments will also change and the annualised rate will also vary.

These new subordinated notes have an indicative distribution of BBSW plus a margin of 220bps to 230bps. The final margin will be determined by a book build, which is a tender process managed by investment banks on behalf of NAB. If recent history is any guide, then the margin is likely to be set at the lower end. Distributions are to be cumulative and paid quarterly in arrears.

The first call date, the date at which NAB can exchange the securities, is on 20 September 2023 and by convention, securities are typically redeemed on this date. Exchange, in the context of listed hybrids, can mean redeem, resell to a third party or convert into ordinary shares. The scheduled maturity date is 20 September 2028.

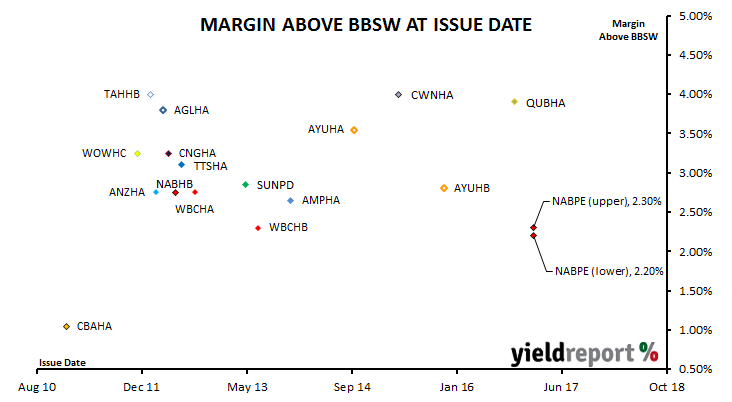

The chart below shows the history of issue margins of ASX-listed notes over the last eight years, including the GFC period in 2008/2009. The new notes are shown at both the lower end of the indicative margin (220bps) and the upper end (230bps).

Issue margins are set with an eye to current market conditions and margins of comparable hybrids already trading. Prices for securities change as soon as trading begins, whether it is on an organised market such as the ASX or an over-the-counter (OTC) market. Other securities issued at different margins may have fallen (or risen) in price, which generally means their trading margin will have changed. The chart below shows the trading margins of comparable securities which trade on the ASX as at the close of business 7 February 2017, as well as the new notes at both the lower and upper ends of the indicative margin range.