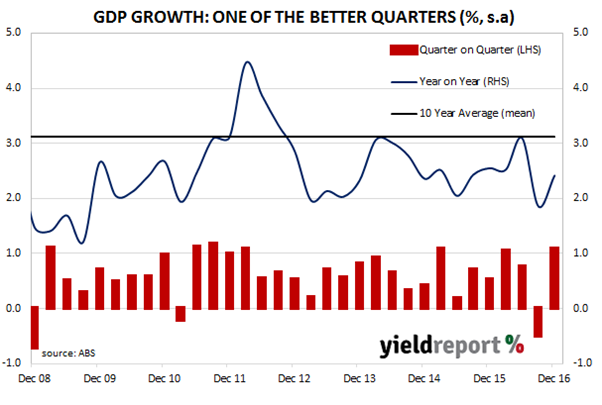

Australia’s negative GDP figure for the September quarter had surprised economists, commentators and investors alike. As a result, there was some apprehension in the lead up to the release of the December numbers. Another negative quarter would have confirmed a recession for Australia, the first since the early 1990s.

Economists had forecast Q4 GDP to be about 0.6%-0.7%. The actual number came in at 1.1% (seasonally adjusted), taking the year-on-year figure up to 2.4%. Unlike the September quarter, public sector investment expanded and added 0.3% of the 1.1% total growth. The bulk of GDP growth came from private consumption expenditures (0.5%) and exports (0.5%) while imports subtracted 0.2%.

Currency markets sent the AUD 0.2 US cents higher and bond yields rose on the day. 3 year bond yields finished 6bps higher at 1.91% and 10 year yields were 8bps higher at 2.83%, although these movements may have been influenced by higher yields in US bond markets overnight.

There was some concern higher consumer spending was at the expense of savings rates. Given a low (and possibly dropping) rate of wage and salary inflation in Australia, consumption spending growth may be difficult to sustain. NAB’s Riki Polygenis counted this as a potential brake on growth in 2018. “We are not as sanguine about growth in 2018 as the RBA…we see a 25bps easing in November 2017 as necessary to prevent a rise in unemployment and inflation undershooting again in 2018.”