By guest contributor Damien McIntyre, CEO, Grant Samuel Funds Management

Duration* is a way to measure a fixed income security’s price sensitivity to interest rates – the longer the duration, the more sensitive it is to interest rate movements. For simplicity, the term bond will be used throughout this article. However, the concepts explored generally apply to all fixed income securities.

Price and yield – an inverse relationship

To understand duration, it’s important to understand the relationship between price and yield. When an investor, be it an individual or an investment manager, buys a bond in the primary market, they are making a loan to the issuer. In return, the bond will be repaid within a specified timeframe and for the term of the loan, regular coupon (interest) payments will be made. If a bond is bought at issue and held through to maturity, the investment will not be affected by changes to interest rates. However, if an investor buys (or sells) a bond on the secondary market, the relationship between the bond’s price and its yield becomes important because price and yield have an inverse relationship. In other words, a bond’s price moves in the opposite direction to its yield.

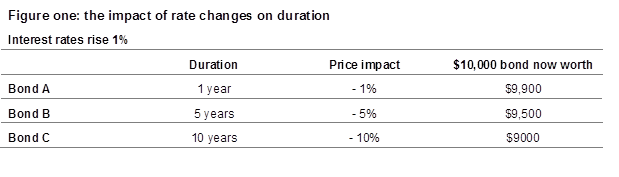

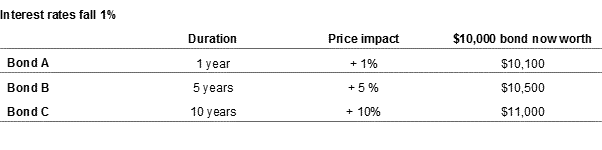

The duration ‘rule’

There is a general rule that applies to duration: for every 1% increase or decrease in interest rates, a bond’s price will change approximately 1%, in the opposite direction, for every year of duration. A low duration indicates that investors will wait a relatively short period to receive the final coupon payment and principal invested. Conversely, a high duration bond will see investors waiting a longer time to receive that final coupon and repayment of principal. The higher the duration, the more a fixed income security’s price will fall with an increase in interest rates. On the other hand, a shorter duration security will experience a lesser fall. This is illustrated by considering the impact of a one percent change in rates (figure one).