In the 1970s and 1980s, inflation rates were often above 5% in Australia. Price increases were routinely factored into wage agreements and rental agreements. Investment forecasting was problematic and high inflation was thought to be an obstacle to new plant and equipment investment. It was not viewed as beneficial to the economy or the people within it.

Nowadays, central banks in advanced economies publicly state their desire for a higher rate of inflation. The sources of inflation are varied. For instance, there is currency debasement (printing money), input cost inflation and wage inflation. However, there is another way to look at the sources of inflation

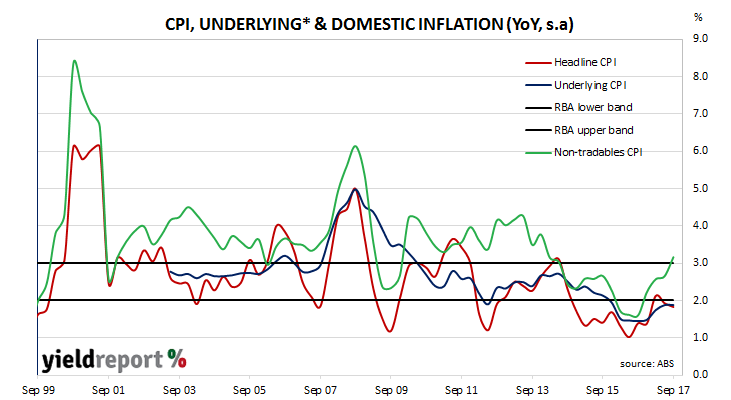

ABS data includes price indices which separates prices of goods and services into “tradables” and “non-tradables”. Tradables are goods and services which can be imported and exported and therefore they compete with goods and services from other countries. Non-tradables, such as haircuts or dry-cleaning are goods and services which cannot be exported and imported. Measures of non-tradables inflation provides a picture of domestic price pressures which can be influenced by domestic monetary and fiscal policies. On the other hand, tradables inflation is influenced by exchange rates, foreign cost structures and pressures which are less dependent of the local economy.

One interesting aspect of recent CPI data is the divergence in the movements of these two components of consumer inflation. Tradables inflation has averaged 1.4% per annum since 1999 but the average for the last five years has only been 0.5% per annum. In the same periods non-tradables inflation has averaged 3.6% per annum and 2.8% respectively. Domestic inflationary pressures eased through 2013 to 2015 but there has been a rebound since June 2016.