Originally published on XTBS.com.au

The objective of diversification is to dampen the effects of a bad outcome of one asset in a portfolio. This can manifest in bonds as either the underperformance of a particular bond compared to the rest of the portfolio or in the worst case, albeit unlikely, the default of any of the issuing companies.

Non-default asset prices

Unlike equities, bonds have both a maturity date and a maturity value. This manifests itself in a known future price of the bond on a known date. We should note that for this section we ignore the possibility of a default – we discuss this later in the article

The impact of having a known future price on a particular date on bond pricing is substantial when compared to equities, which can triple or quarter in value. Because a bond must finish at a certain price on a certain day, it makes it difficult for bond prices to deviate too much from that particular future value. Naturally, the further you are from that date the more the price can deviate. It is this feature which gives bonds inherently lower volatility than equities.

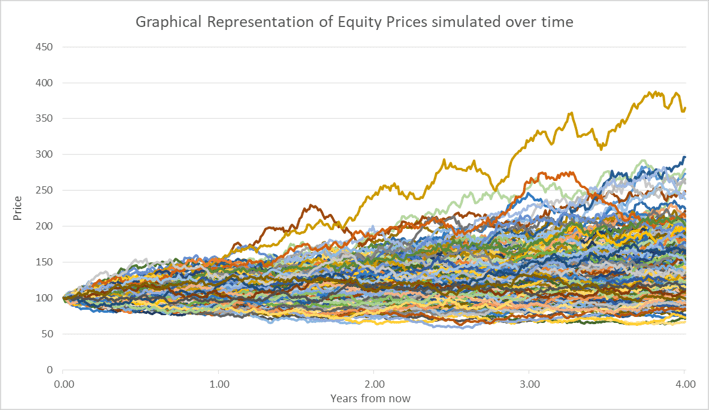

To illustrate this, we take market data from both the S&P/ASX 200 and the Bloomberg AusBond Credit 0+ Yr Index – both of which are used to describe generally their underlying markets. We then use this information to perform 250 simulations of the potential prices of an “average equity” and 250 simulations of potential prices of the “average bond”. Both charts are based over a 4-year horizon.

Chart 1: 250 Equity Price Simulations

Note: This chart is a graphical simulation of how equity prices may behave, based on model assumptions and calibrated historical data. It may not reflect actual price movements of any particular equity.