Italian federal elections were held in early March, over two months ago. Due to the absence of an outright majority by any one party in the lower house of the Italian parliament, no new government was immediately formed.

The world has become accustomed to a higher level of instability in Italy’s federal politics. Short-lived Italian governments have been almost the norm since 1945 and some delay in the formation of a coalition in order to form a government after elections was not perceived as particularly disturbing. Italy’s bond market continued business as usual and yields were not especially volatile.

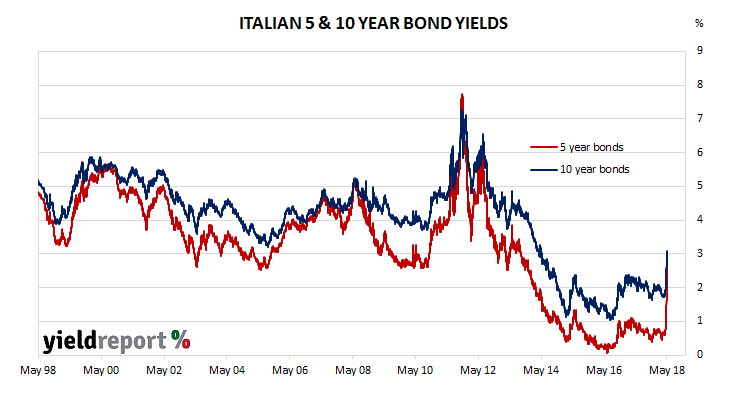

The yield on Italian 10 year bonds started March at just under 2%. It reached a March peak at 2.01% in the middle of the month and then it drifted lower and settled in a 1.70%-1.80% range for most of April.

It stayed there until the second week of May. The parties with the most seats, the Five Star Movement and the League, appeared to have formed a coalition but doubts arose as to whether such a government would adhere to European Union rules regarding fiscal policy. Bond yields started to increase by larger-than-normal daily amounts.

A proposal to issue vouchers, or “mini-BOTs” as they became known, exacerbated investors’ fears. The proposal was reportedly part of the Five Star-League Accord as a way to settle debts with Italian taxpayers. The vouchers would be used to pay tax and buy goods and services from government organisations and government-owned businesses. They would pay no interest and have no maturity date, so in some ways, they appeared to share some characteristics with cash. Some saw the proposal as a way to issue a parallel currency which could keep functioning should Italy choose to leave the eurozone.