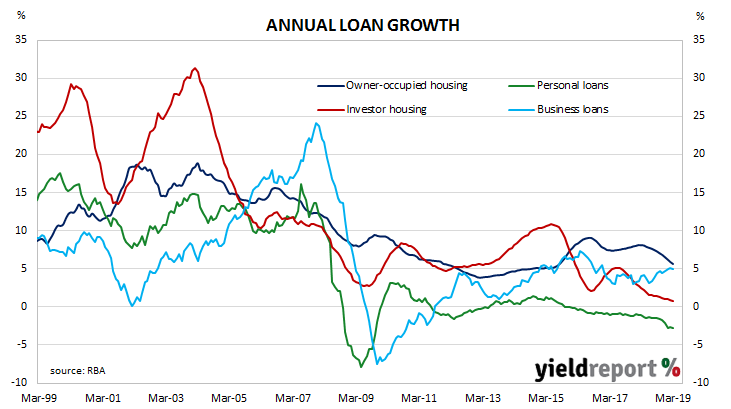

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but credit figures in the December quarter put paid to that idea. The latest figures confirm the first quarter of calendar 2019 has provided more of the same.

According to the latest RBA figures, private sector credit grew by 0.3% in March, the same growth rate as in February and in line with the 0.3% consensus estimate. However, the annual growth rate slipped from February’s revised figure of 4.1% to 3.9% as home and business lending continued to slow and personal lending further contracted.

The figures were largely as expected and the reaction of markets was minimal. By the end of the day, the yield on 3-year Treasury bonds had slipped 1bp to 1.26%, the 10-year yield remained unchanged at 1.80% and 20-year yields had inched up 1bp to 2.26%, largely ignoring an overnight increase of US Treasury bonds. Expectations of a rate cut remained largely unchanged. The implied probability of a rate cut at the RBA’s May Board meeting remained at 36% while an August cut is entirely factored in. By November, one rate cut is expected with another cut on top viewed as an 84% chance.

ANZ senior economist Cherelle Murphy said, “The housing credit impulse fell further in March, consistent with further declines in house prices. We expect housing credit to continue to be weak, as tighter credit conditions which led to the decline in house prices pass through the system. Although business credit growth saw a slight bounce in March, based on forward-looking loan approvals, we expect business credit to remain subdued.”

Andrew Hassan, a senior economist at Westpac, was in general agreement. “For private sector credit, it’s a case of another month, another soft update. Credit growth has moderated to a slow pace led by the housing downturn.” However, he noted “the pace of decline for the housing sector appears to have eased early in 2019.”