Sponsored Content

By Anujeet Sareen CFA, Portfolio Manager, Brandywine Global

- In this two-part series, we start by proposing the bullish case for global growth and follow up with the bear case, along with our investment outlook.

- In prior global recessions, synchronised monetary tightening and a major misallocation of capital have often pushed the economy into recession. We don’t see a potent combination of these factors right now.

- The current global expansion hasn’t seen a boom that is usually a precondition for a bust in the cycle.

- Policymakers around the world are expected to implement fiscal stimulus to support economic growth.

This June, the current economic expansion will end up being the longest in post-war history. Therefore, it’s natural to ask, “Are we headed into a recession later this year or in 2020?” It’s a tall ask to evaluate whether a global recession is coming and a logical place to start is by understanding where we are in the global economic cycle because that has investment implications. This article – Part 1 – outlines the bull case for global growth and Part 2 analyses the bear case and explains how the data informs our investment thesis and outlook.

The bullish view of the global economic cycle

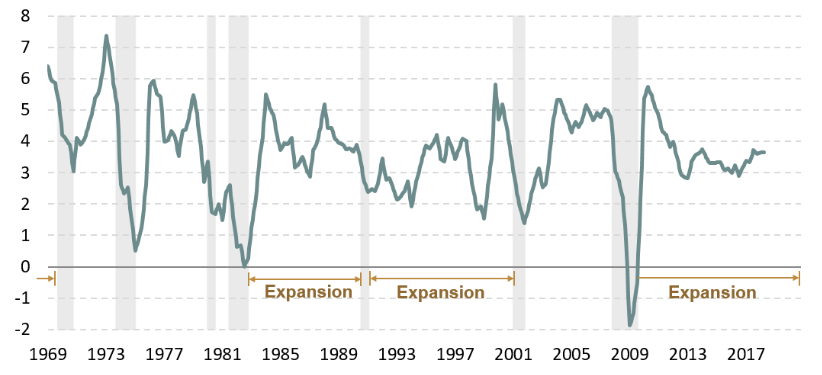

The bullish argument starts with the observation that economic cycles don’t end simply because they get old. For example, the economies of Japan, Australia, Sweden and Italy did not experience recession in the immediate post-war period from 1948-1973, although this entire period was not captured below (see Chart 1).

Chart 1: Global real GDP growth (recessions shaded, annual % change)

Source: IMF/Have Analytics, June 2018