By guest contributor Atchison Consultants

Australia’s superannuation system was introduced to the general population in the early 1990s. Since then, total assets in the sector have grown from very little to around $2.7 trillion. In that time, Australians’ investment preferences have shown a marked tendency towards certain types of assets. A recent study by the Thinking Ahead Institute, a Willis Tower Watson think tank, shows just how different Australia is to the rest of the world and it also offers a clue as to why the difference has emerged.

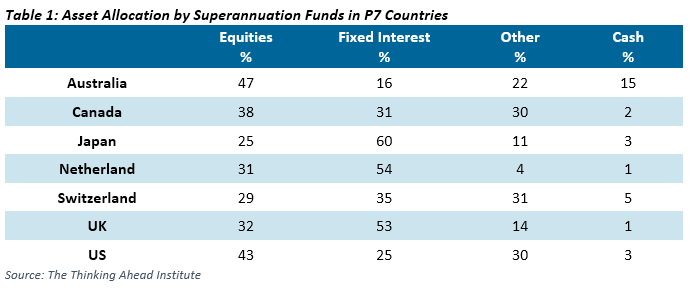

The study was across global pension assets at the end of 2018 and it looked at some of the differences in growth rates, assets-to GDP ratios and asset allocation of the “P7” countries. P7 countries comprise the seven major pension markets in the world; Australia, Canada, Japan, Netherlands, Switzerland, UK and US.

A comparison of Australian pension assets with the average asset allocation profiles of other P7 markets illustrates some large differences. Table 1 sets out P7 countries’ asset allocations. The “Other” category comprises a wide range of assets including property, infrastructure, hedge funds and private equity.

One obvious message is that the allocation to fixed interest in Australia is relatively low. Another is that two countries, Australia and the US, have relatively high exposure to equities when compared to the rest of the P7 markets. Both the US and Australia have a significant majority of defined-contribution funds.