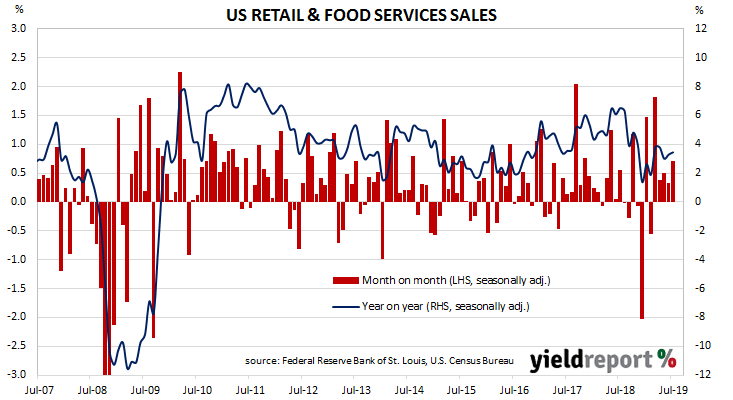

US retail sales had been trending up since late 2015 but, beginning in late 2018, a series of weak or negative monthly results led to a drop-off in the annual growth rate which brought the annual rate below 2.0% by the end of the year. After an unsteady start to 2019, subsequent months’ figures have produced a recovery which has prevailed into the third quarter of the year.

According to the latest “advance” sales numbers released by the US Census Bureau, total retail sales increased by 0.7% in July, well in excess of the +0.2% which had been expected and well above June’s revised growth rate of +0.3%. On an annual basis, the growth rate increased to 3.4% from June’s revised rate of 3.3%.

Treasury bond yields finished the day noticeably lower despite the better-than-expected results from the retail report, as traders and investors focussed on Chinese plans for retaliation on the trade front, along with a weak industrial production report and hints of some move at the ECB’s September meeting. By the close of business, 2-year US Treasury yields had dropped by 9bps to 1.49%, the 10-year yield had shed 6bps to 1.52% while 30-year yields finished 5bsp lower at 1.97%.