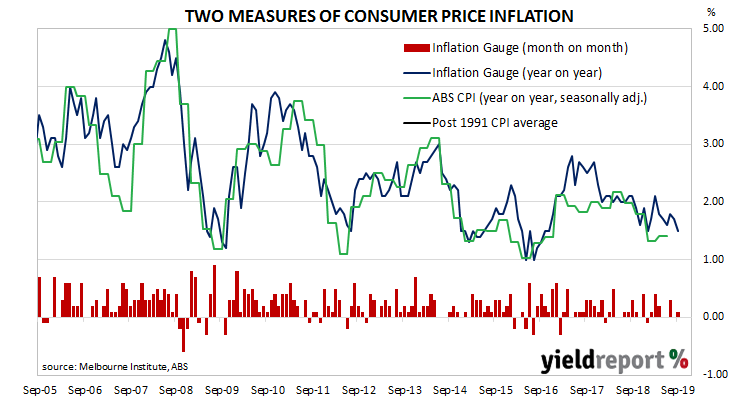

The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, its attempts to accelerate inflation through record-low interest rates have failed so far. The latest unofficial measurement of consumer inflation is unlikely to provide Australian policy makers with new evidence of inflationary pressures.

The Melbourne Institute’s latest Inflation Gauge index increased by 0.1% in September after a flat result in August and a 0.3% increase in July. On an annual basis, the index increased by 1.5%, slowing from August’s 1.7%.

Despite slightly lower US Treasury yields in overnight trading, local yields increased noticeably, although August’s bank lending figures will have had some bearing. By the end of the day, 3-year ACGB yields had increased by 3bps to 0.70% while 10-year and 20-year yields had both jumped by 7bps to 1.01% and 1.43% respectively.