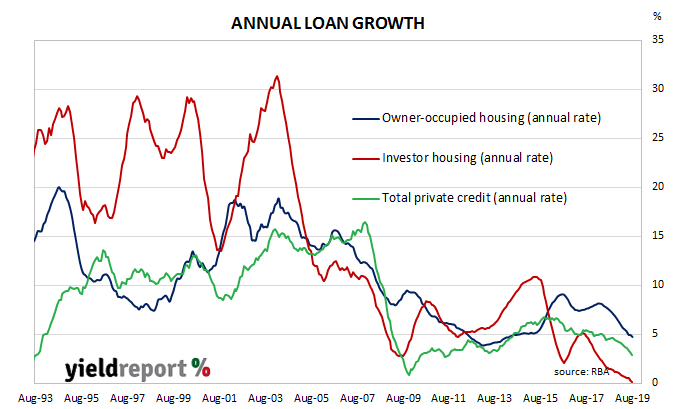

The pace of lending to the non-bank private sector by financial institutions in Australia has been trending down since October 2015. It appeared to have stabilised in the September quarter of 2018 but then subsequent credit figures put paid to that idea. Despite some optimism emerging in the housing market following the re-election of the Coalition Government in May, lending figures are not indicative of any rush in recent months to draw upon finance facilities.

According to the latest RBA figures, private sector credit grew by 0.2% in August, less than the expected +0.3% but the same as July’s +0.2%. Once again, the annual growth rate slipped, this time from July’s figure of 3.1% to 2.9%. Lending to owner-occupiers and business remained subdued while investor lending moved a little closer to going into a contraction. Despite slightly lower US Treasury yields in overnight trading, local yields increased noticeably, although the Westpac-Melbourne Institute’s latest Inflation Gauge may have muddied the waters to some degree. By the end of the day, 3-year ACGB yields had increased by 3bps to 0.70% while 10-year and 20-year yields had both jumped by 7bps to 1.01% and 1.43% respectively.

Despite slightly lower US Treasury yields in overnight trading, local yields increased noticeably, although the Westpac-Melbourne Institute’s latest Inflation Gauge may have muddied the waters to some degree. By the end of the day, 3-year ACGB yields had increased by 3bps to 0.70% while 10-year and 20-year yields had both jumped by 7bps to 1.01% and 1.43% respectively.

Prices of cash futures contracts were largely unmoved by the report and a rate cut was still expected in the short term. By the end of the day, October contracts implied a 79% chance of a 25bps rate cut, the same as on the previous day, while November contracts still fully factored in one rate cut plus a 14% chance of another cut as well.

The traditional driver of loan growth rates, the owner-occupier segment, slowed to +0.3% in August from July’s +0.5%. Its 12-month growth rate also slowed as it fell back to 4.7% after recording 4.9% in July.