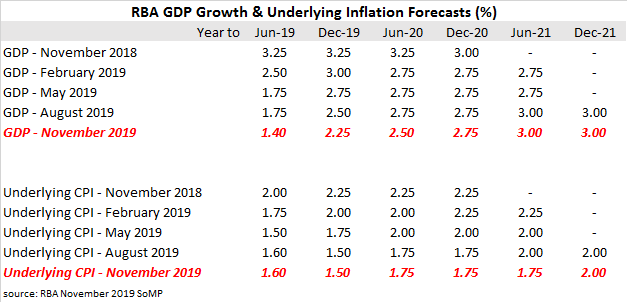

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for the updates to the RBA’s own forecasts. In February’s SoMP, the opening statement of the “Outlook” section stated “Domestic economic conditions have been a bit softer than were expected at the time of the November Statement.” In May, this was changed to “Economic growth in Australia was weaker over 2018 than expected at the time of the February Statement.” August’s SoMP continued this theme of weakness. “Domestic economic growth in the first half of the year was a little lower than expected at the time of the May Statement.” However, conditions appear to have stabilised over the last three months and November’s Outlook starts with “The outlook for the Australian economy is little changed since the August Statement.” As a consequence, the RBA has largely left its forecasts unchanged except for a tweak here and there.

GDP growth in the early periods of the RBA’s forecasts though to June 2020 (see table) have been reduced by 0.25% (year to December 2019 and year to June 2020) but later periods have been left unchanged. Note the latest forecast for the year to June 2019 has been downgraded by 1.85% over the last 12 months.

The RBA’s underlying inflation forecasts were left unchanged. September quarter inflation “was as expected” at the time of the August SoMP. The RBA anticipates inflation “a little over the forecast period” as spare capacity is eroded and GDP growth returns “to above potential.” The RBA’s favoured measure of underlying inflation, the “trimmed mean”, was expected to rise to 2.0% by June 2021 but this expected increase has been deferred for six months until December 2021.