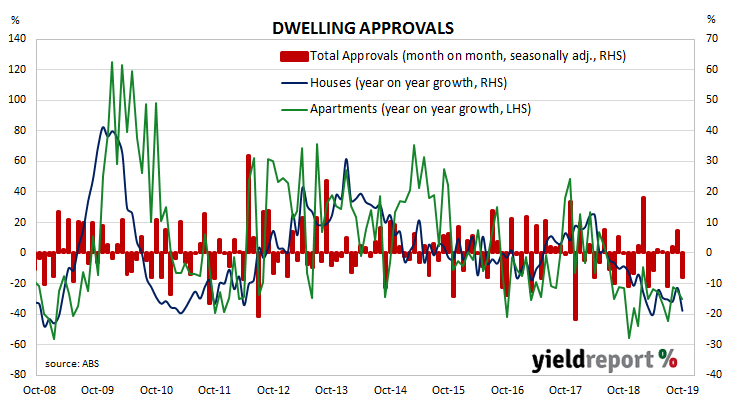

Approvals for dwellings, that is apartments and houses, have been heading south since mid-2018. As an indicator of investor confidence, falling approvals represent a worrying signal, not just for the building sector but for the overall economy. There had been some expectation of a recovery in recent months but economists now appear uncertain.

The Australian Bureau of Statistics has now released the latest figures from October and total residential approvals dropped by 8.1% on a seasonally-adjusted basis, a larger fall than the 1% decrease which had been expected and a large turnaround from September’s revised figure of +7.2%. On an annual basis, total approvals fell by 23.6%, a marked deterioration from September’s comparable figure of -17.0% after revisions.

Westpac senior economist Matthew Hassan said, “The detail was particularly disappointing; rather than a high-rise driven result, weakness was more evenly spread across all dwelling types…”

Domestic bond yields finished the day noticeably higher, although it is unlikely the sell-off was driven by this report, ANZ’s latest Job Ads survey or the latest Inflation Gauge report. By the end of the day, 3-year ACGB yields had gained 4bps to 0.69% while 10-year and 20-year yields had each increased by 6bps to 1.10% and 1.50% respectively.

Prices of cash futures contracts moved to lower expectations of another cut in the cash rate target, although one more rate cut is still largely expected within the next six months. By the end of the day, December contracts implied a 9% chance of another 25bps rate cut, down from the previous day’s 13%. February contracts implied a 70% chance of a cut, down from 77% while May continued to fully price in another rate reduction.