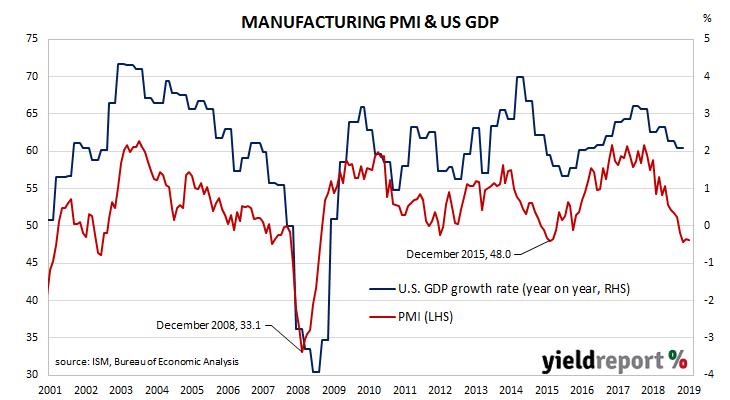

US purchasing managers’ indices (PMIs) have been sliding since August 2018, albeit from elevated levels. After reaching a cyclical peak in September 2017, manufacturing PMI readings went sideways for a year before they started a downtrend. However, readings appear to have stabilised lately, albeit at sub-neutral levels.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 48.1 for November, slightly less than October’s reading of 48.3 and less than the market’s expected figure of 49.5. The average reading since 1948 is 52.9 and any reading below 50 implies a contraction.

The ISM’s Tim Fiore said, “Global trade remains the most significant cross-industry issue. Among the six big industry sectors, Food, Beverage & Tobacco Products remains the strongest, while Fabricated Metal Products is the weakest.” NAB economist Tapas Strickland said a fall in the New Orders sub-index is “suggestive that activity could weaken further in the months ahead.” ANZ senior economist Cherelle Murphy said the figures “suggest US manufacturing activity is still struggling.”

US Treasury yields increased along the curve, especially at the long end. By the end of the day, 2-year Treasury bond yields had inched up 1bp to 1.61%, the 10-year yield had increased by 4bps to 1.82% and the 30-year yield finished 7bps higher at 2.27%.

In terms of likely US monetary policy, according to federal funds futures contracts the probability of another rate cut in 2019 remained at zero. The likelihood of a 25bps cut at the January meeting of the FOMC declined a little, moving from 10% to 8%. A move in March is also viewed as unlikely, although the implied probability had increased from 18% to 20% by the end of the day.