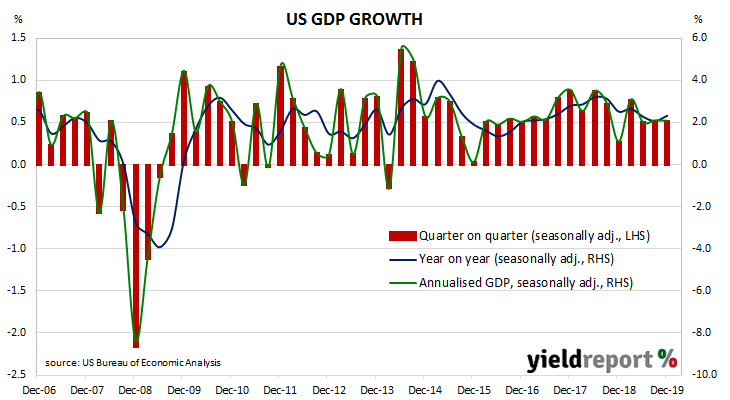

While the US has a historically low unemployment rate, recent bond yields suggest future growth rates will be below trend. The US Fed agreed and it reduced its federal funds range three times in the second half of 2019 as a form of insurance against a softening economy. While US GDP growth slowed in the second quarter of that year, it stabilised and then maintained a 0.5% per quarter growth rate.

The US Commerce Department has just released December quarter “advance” GDP estimates and they indicate the US economy grew at 0.5% for the quarter or at an annualised growth rate of 2.1%. The growth figure was a touch higher than the 2.0% which had been expected but it was the same as the September quarter’s final figure.

ANZ senior economist Cherelle Murphy said, “The private domestic demand components of GDP softened. Waning fiscal stimulus, capacity constraints and trade policy are weighing on growth.”

US Treasury bond yields moved lower. By the end of the day, the 2-year Treasury bond yield had lost 4bps to 1.37%, the 10-year yield had shed 5bps to 1.53% while the 30-year yield finished only 2bps lower at 2.01%.

In the futures market for federal funds, expectations of another cut in the first half of 2020 hardened albeit from a low base. According to end-of-day prices, the implied probability of a 25bps rate cut at the FOMC’s March meeting was 13%, up from the previous day’s 7%. The implied probabilities of a cut at the April and June meetings was 25% and 44% respectively.