The market awoke to the news that Australia has its fifth Prime Minister in five years with Malcom Turnbull challenging Tony Abbott for the job and winning the party vote. Australia is becoming used to cutting down Prime Ministers and markets took the news in their stride. The joke doing the rounds was that the Richmond Football Club, an AFL club famous for sacking coaches, has had only one coach in the same period!

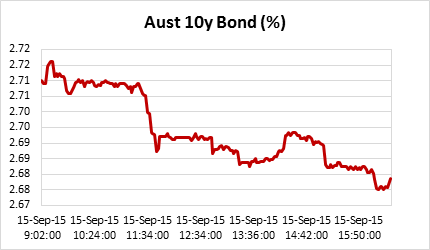

The move to a new PM saw 10y bond rates rise a couple of basis points as the new PM is seen as business positive and with rhetoric themed around kick-starting the economy. This was swiftly reversed after the RBA minutes were released at 11:30am as can be seen in the chart below of the day’s trading. The minutes of the September RBA board meeting were seen as decidedly “dovish” and long bond rates reversed the early morning trend to fall 2bps. The AUD also dropped against the USD.

Westpac’s Bill Evans said, “The minutes of the monetary policy meeting of the Reserve Bank Board for September provided no real surprises…it would appear that the Bank is now reasonably comfortable with the degree of adjustment of the AUD.” He went to say the RBA is “still not giving any encouragement” to a market expecting a rate cut by November.

JP Morgan’s Stephen Walters said the minutes revealed the chances of further reduction in the official cash rates was slim. “It likely would take more profound disappointments in markets or in conditions in Australia’s major trading partners, alongside domestic deterioration, including a higher jobless rate,” he said.

AMP Capital’s Shane Oliver noted how APRA’s lending restrictions on investment housing may mean the housing market is less of a constraint on rates but added there was nothing really new in the minutes.

The RBA minutes can be summed up as follows:

- Increased household expenditure and the depreciation of the Australian dollar were expected to produce growth in non-mining investment.

- Forward looking indicators of conditions pointed to the unemployment rate remaining around current levels.

- Mining investment appears is expected to weaken further than previously expected.

- Non mining investment was expected to fall further but a slower than previously anticipated rate.

- APRA’s measures had slowed the growth in lending for investment housing, Sydney remains buoyant but the rest of Australia house price inflation had been modest or even negative.