The RBA’s stated objective is to achieve an inflation rate of between 2% and 3%, “on average, over time.” Since the GFC, Australia’s inflation rate has been trending lower and lower and it has been below the RBA’s target band for some years now. Despite the RBA’s desire for a higher inflation rate, attempts to accelerate inflation through record-low interest rates have failed so far.

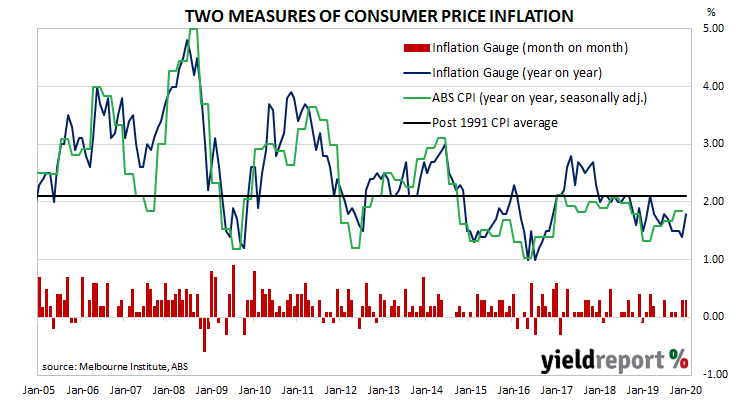

The Melbourne Institute’s latest Inflation Gauge index increased by 0.3% during January following a 0.3% increase in December and a flat result in November. On an annual basis, the index increased by 1.8%, up from December’s 1.4%.

Domestic bond yields finished a little lower, largely ignoring significant overnight falls in US markets. By the end of the day, 3-year and 10-year ACGB yields had each lost 3bps to 0.58% and 0.94% respectively while the 20-year yield had shed 2bps to 1.33%.

Expectations of another cut in the cash rate target hardened. By the end of the day, February contracts implied a 28% chance of a 25bps rate cut, up from the previous day’s 14% while March contracts implied a 62% chance of a cut, up from 44%. Prices of April contracts had a rate cut fully built-in.