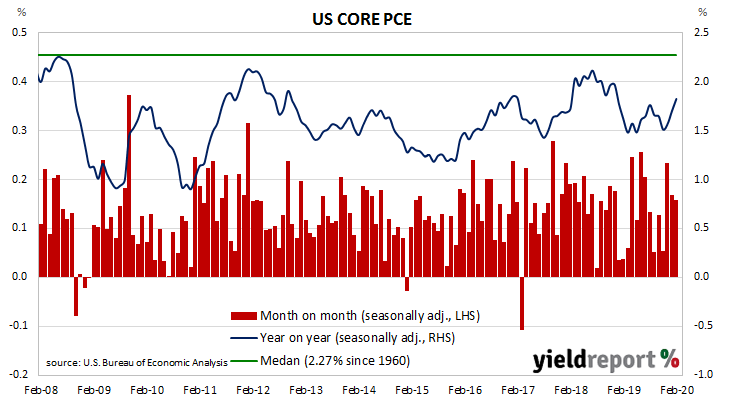

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% through to the end of 2018 before dropping in the first quarter of 2019 to around 1.5%. It has ranged between 1.5% and 1.8% since then.

The latest figures have now been published by the Bureau of Economic Analysis as part of the March personal income and expenditures report. Core PCE prices decreased by 0.1% for the month, in line with a -0.1% which had been expected but lower than February’s 0.2% increase. On a 12-month basis, the core PCE inflation rate ticked down from February’s figure of 1.8% to 1.7%.

ANZ economist Kishti Sen said, “As demand collapses…there will be more deflation to come in the months ahead.”

US Treasury yields finished higher at the long end despite “risk-off” moves by investors away from equity markets. By the end of the day, the 2-year Treasury yield had slipped 1bp to 0.19% while the 10-year yield had inched up 1bp to 0.64% and the 30-year yield had increased by 3bps to 1.28%.

In terms of US Fed policy, a rate change of any sort remained unlikely given the federal funds rate has been at the effective lower bound since the US Fed reduced it on Sunday 15 March. However, contract prices out to March 2021 imply traders think there is a small chance of a 25bps increase in the federal funds rate beginning in December.