Summary: Home loan approvals fall in number but increase in value over March; owner-occupier loans rise; investor loans decline.

A very clear downtrend was evident in the monthly figures of both the number and value of home loan commitments through late-2017 to mid-2019. Then the RBA reduced its cash rate target in a series of cuts and both the number and value of mortgage approvals began to noticeably increase. Figures from February provided an indication the trend may have finished but the latest figures still do not provide some sort of confirmation.

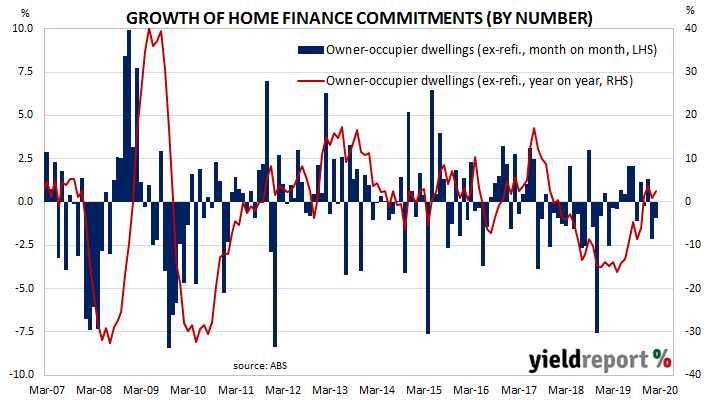

March’s housing finance figures have been released and the total number of loan commitments (excluding refinancing loans) to owner-occupiers fell by 0.9%, a slower contraction rate than February’s revised figure of -2.1%. However, on an annual basis, the growth rate increased from February’s revised figure of 0.9% to 2.5%.

Westpac senior economist Matthew Hassan said, “This is a throwback to pre-coronavirus [times], reflecting the strength of conditions earlier in the year.” The report came out on the same day as March retail sales figures and Commonwealth bond yields moved higher, largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had ticked up 1bp to 0.25% while 10-year and 20-year yields had each gained 5bps to 0.91% and 1.53% respectively.

The report came out on the same day as March retail sales figures and Commonwealth bond yields moved higher, largely in line with US Treasury movements. By the end of the day, the 3-year ACGB yield had ticked up 1bp to 0.25% while 10-year and 20-year yields had each gained 5bps to 0.91% and 1.53% respectively.

In the cash futures market, expectations of a rate cut softened a little. By the end of the day, June contracts implied a rate cut down to zero as a 51% chance, down from the previous day’s 54%. July contracts implied a 65% chance of such a move in that month, down from 67%. Contract prices of months in the remainder of 2020 and through to mid-2021 implied similar probabilities, ranging between 43% and 60%.