Summary: US output drop larger than March fall; at GFC level; capacity utilisation hits 50-year low.

The Federal Reserve’s industrial production (IP) index measures real output from manufacturing, mining, electricity and gas company facilities located in the United States. These sectors are thought to be sensitive to consumer demand and so some leading indicators of GDP use industrial production figures as a component.

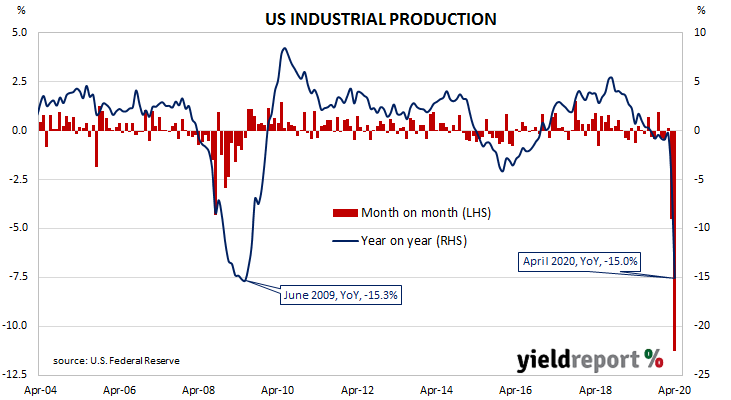

Figures from early-2020 had been suggestive of a possible end to a downtrend which began in late-2018. However, the latest report makes March’s awful figures seem relatively “good”.

According to April figures, US industrial production contracted by 11.2%, roughly in line with the -11.4% which had been expected but also a severe deterioration from March’s revised figure of -4.5%. On an annual basis, the growth rate plunged from March’s revised figure of -4.9% to -15.0%.

The report came out on the same day as reports on retail sales, job openings (JOLTS) and consumer sentiment. US Treasury bond yields finished higher; the US 2-year Treasury yield remained unchanged at 0.15% while 10-year and 30-year yields both finished 4bps higher to 0.65% and 1.33% respectively.

In terms of US Fed policy, expectations of any change in the federal funds rate over the next 12 months remained fairly soft. However, OIS contracts from March 2021 onwards continued to imply a zero effective federal funds rate even after US Fed chief Jerome Powell recently repeated the Fed’s reluctance to embrace negative rates.