Sponsored Content

Dino Rebellato, Investor Relations Manager, Millbrook Group

A wise fixed income investment manager once expressed to me the following opinion: “When you drill right down, all debt investments are really insurance policies. Which side do you want to be on?”

While people in financial markets understand (or should understand) the notion of “put options”, very few boil them down to their essence – insurance policies. For example, with “high yield” bonds, the investor is the insurer, receiving small “premiums” in the form of interest payments while occasionally having to pay out in the event of default. Nassim Nicholas Taleb, author of “The Black Swan”, described such strategies as “picking up pennies in front of a steam roller”. We have these investments produce attractive returns but we have also seen what happens when the steam roller suddenly hits a downhill run, taking out the languishing penny collectors in the process. The damages incurred are termed “losses given default” and may be very high depending on the investor’s position in the queue (seniority) when debtors are paid out.

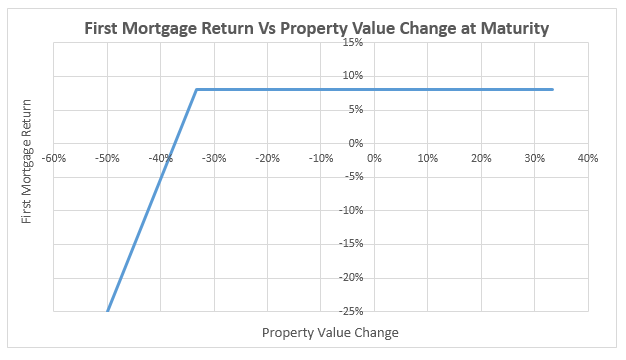

First mortgages can also be seen as a form of insurance. However, they are different from other debt investments because they provide an additional level of protection to investors. This works like a protective put option to a specific point of loss. A put option is a contract that pays you out in the event of default – just like an insurance policy. With first mortgages, real protection is the amount of collateral or equity. Let’s look at an example of how this works.

By lending to a borrower and taking the first mortgage as collateral, the borrower is contracted to pay the lender an agreed interest rate and a principal payment upon maturity. The lender can limit the potential for losses given default by ensuring borrowers not only have the capacity to pay interest but enough equity in their mortgaged property that ensures that the amount owed is covered to an acceptable level. The following graph illustrates the pay-off for a typical mortgage where $1 million is loaned for 12 months on a property valued at $1.5 million (loan-to-value ratio: 66%) at an interest rate of 8%.