Summary: Prices received by producers fall on average; decrease more than expected; driven by lower services prices; core PPI near zero; excess capacity behind “disinflation”.

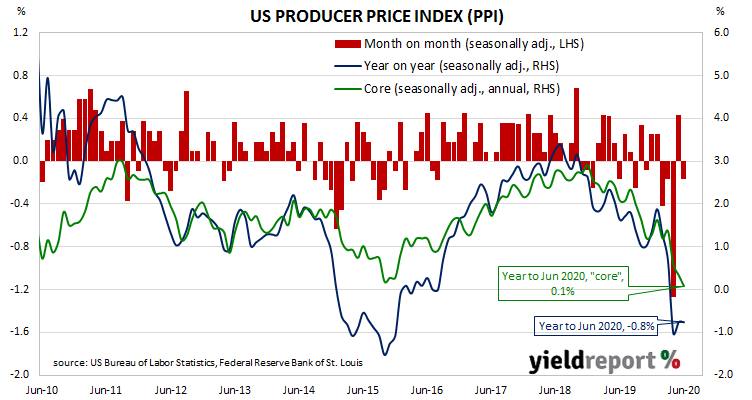

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which then continued through 2019. Months in which prices received by producers increased suggested the trend may have been coming to an end, only for it to continue. The downtrend turned into a plunge in April.

The latest figures published by the Bureau of Labor Statistics indicate producer prices fell by 0.2% after seasonal adjustments in June. The decrease was in contrast to the 0.4% rise which had been generally expected and May’s +0.4%. On a 12-month basis, the rate of producer price inflation after seasonal adjustments remained negative at -0.8%, the same rate as in May but higher than April’s -1.0%.

“Core” PPI inflation fell by 0.3%, a larger decline than May’s -0.1%. The annual rate fell again, this time from 0.3% to 0.1%.

Westpac’s Finance AM team said, “There obviously are no upside pressures building…” They also noted FOMC member Robert Kaplan had recently said the US would experience “disinflation for some period of time until we get rid of this excess capacity”.

Despite the lower-than expected figures, US Treasury bond yields finished moderately higher at the long end. By the end of the day, the US 2-year yield remained unchanged at 0.16% while the 10-year yield had gained 3bps to 0.64% and the 30-year yield had increased by 2bps to 1.34%.

The BLS stated lower prices for final demand services were the main drivers of the month’s decline after they decreased by 0.3% on average. Prices of goods increased by 0.2% on average.