Sponsored Content

Dino Rebellato, Investor Relations Manager, Millbrook Group.

A well-worn saying to justify remaining invested in equities during volatile times is “Don’t fight the Fed” (the US Federal Reserve Bank). You can now substitute most central banks and many supra-national government agencies, bodies which could be referred to as the “great intermediators”, for the Fed. In effect, ‘There shall be liquidity” appears to have become our eleventh commandment, alongside “Thou shalt not kill” and nine others.

Today, almost all investments comprise very liquid assets. These include the obvious ones – listed equities, debt and derivatives. Furthermore, the investment banking community has made an art from of transforming illiquid, low-scale assets into securitised and risk-tranched pools available to investors both large and small. In doing so, everything looks “liquid”. Like any feature, liquidity has a price for which the originator, normally the investment bank, is handsomely rewarded from a presumably satisfied end-investor. Of more concern in the modern era is that most liquid assets now behave as proxies for the policies associated with the eleventh commandment, “There shall be liquidity”.

The flip side is that this liquidity is reflected in market volatility, the roller coaster of price fluctuations that cause certain risk-averse investors sleepless nights. That eleventh commandment, “There shall be liquidity”, remains the great uncertainty for those who remain sceptical of the capacity for unlimited support of financial institutions and the liquid assets that support their balance sheets.

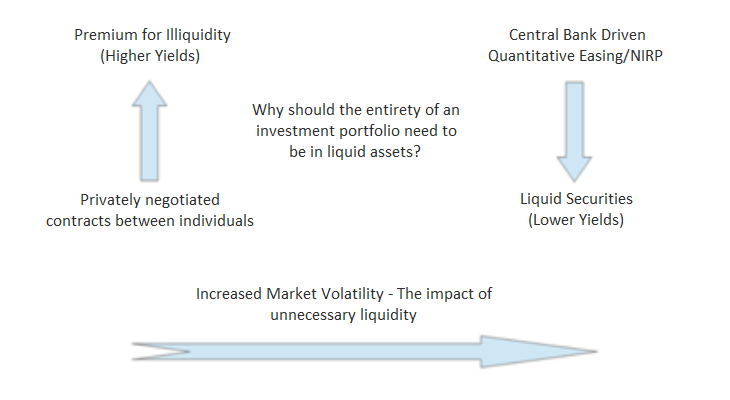

How can investors separate themselves from the influence of central bankers, the great intermediators? The answer is in private contracts between consenting parties. This is where private debt, in particular first mortgages, can play a critical role.

Traditionally strategies are constructed on the basis of optimised risk and return. Let’s recast this idea in terms of optimisation of “fiat liquidity” (assets dependent on government/central bank support) and “independently controlled contracts” (assets whose maturity and return on and of capital is defined between consenting parties). It is worth thinking about first mortgages, as well as other forms of private debt, as not easily tradeable but occasionally liquid securities. With the prevalence of interventions by central banks and governments designed to support struggling banks and companies, savers are suffering. The mainstream approach to enhancing yield is to take on more risk in liquid assets, an approach that concentrates more risk in the same asset classes at most risk of central bank and government interventions. The following graphic illustrates the trade-off between returns and fiat liquidity.