Summary: Prices received by producers increase by 0.4% on average in September; rise noticeably higher than expected; annual “core” PPI rate doubles (from low base); long-term US bond yields unchanged on day; PPI rise driven equally by goods and services prices.

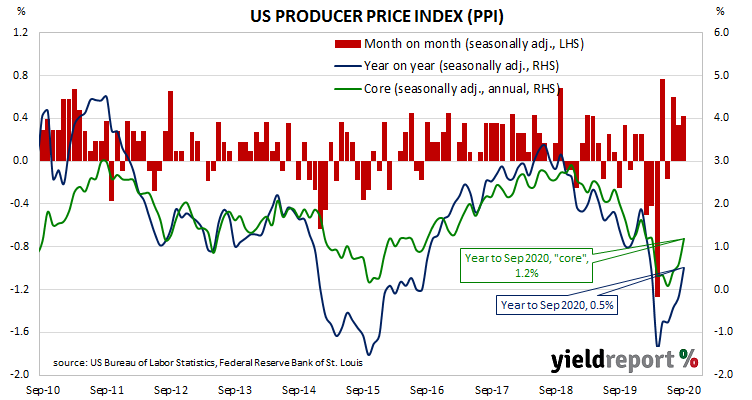

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which then continued through 2019. Months in which prices received by producers increased suggested the trend may have been coming to an end, only for it to continue, culminating in a plunge in April. Figures from subsequent months suggest a return to “normal” may be taking place.

The latest figures published by the Bureau of Labor Statistics indicate producer prices rose by 0.4% after seasonal adjustments in September. The increase was noticeably above the 0.1% rise which had been generally expected and a little higher than August’s 0.3% rise. On a 12-month basis, the rate of producer price inflation after seasonal adjustments increased to 0.5%, up from the -0.2% annual rate recorded in August.

“PPI inflation is still adjusting to the volatility of the COVID-19 crisis, but at 0.4% is not enough to fuel inflation,” said ANZ economist John Bromhead.

PPI inflation excluding foods and energy rose by 0.4% after recording increases of 0.4% in August and 0.5% in July. The annual rate doubled from August’s 0.6% to 1.2%. US Treasury bond yields were unresponsive to the report. By the end of the day, 2-year, 10-year and 30-year yields were all unchanged at 0.14%, 0.73% and 1.51% respectively.

The BLS stated higher prices for final demand services accounted for two-thirds of the month’s increase after they rose by 0.4% on average. Prices of goods also increased by 0.4% on average.