By guest contributor Brad Dunn, Senior Credit Analyst, Daintree Capital

In these times where every basis point counts, hybrids stand tall, offering the highest yields for an investment-grade credit rating. As a reminder, a credit rating is simply an opinion of the likelihood that a bond will default during its time on issue.

While hybrids are attractive on a gross yield or spread basis, there is no such thing as a free lunch. These higher relative returns come with a catch – complexity.

The liability side of a bank balance sheet is multi-layered, ranging from super-senior instruments and customer deposits that are highly protected at the top of the stack, through to hybrid securities that sit just above shareholders equity. The compensation on offer to securities at each level generally reflects their seniority, but can be influenced by any number of other factors.

Table 1: Bank funding profile

Typical bank funding profile (ranked by seniority)

Covered Bonds (Cash + 20-40bp)

Senior Bonds (Cash + 30-60bp)

Subordinated Bonds (Cash + 120-200bp)

Hybrid Securities (Cash + 250-500bp)

Equity (8-10% pa)

source: Daintree estimates

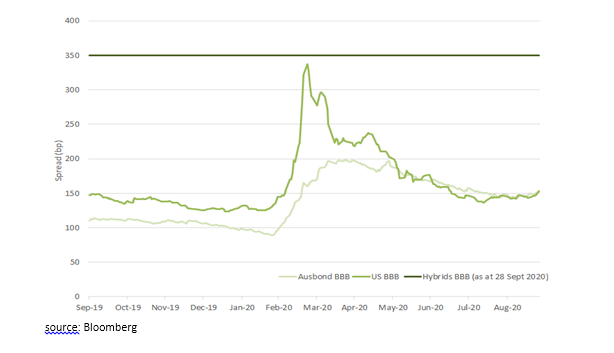

The real attractiveness starts to show through when you compare hybrid yields to corporate bonds with the same credit ratings. We compare hybrid spreads to two indices of BBB-rated corporate bonds, one Australian and one American. We have set the hybrid curve to current spreads, inclusive of franking credits where available.

The chart below shows a clear spread advantage to hybrids with a BBB rating. Even in the turmoil of COVID-19 where credit spreads widened quickly and dramatically, the US BBB index did not reach the spread levels that Australian hybrids have subsequently reverted to. For context, Australian hybrid spreads widened to as high as 700bps over cash for a short period as liquidity dried up.

Figure 1: BBB spreads